EU HEALTHCARE: Healthcare: Week in Review

Feb-07 13:51

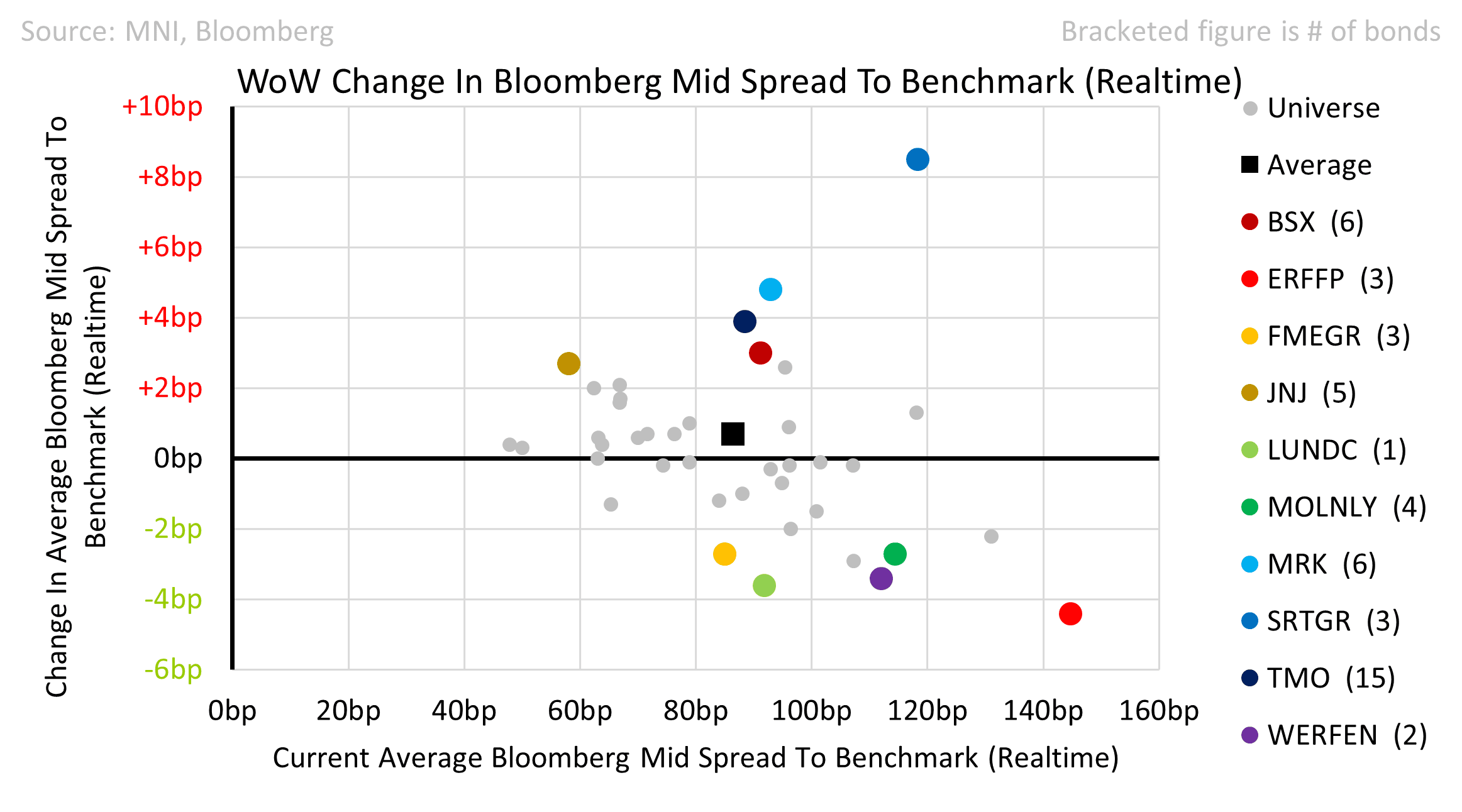

- Becton Dickinson announced plans to spin-off part of its Life-Science business. Roughly 12% of total earnings affected. The equity reacted poorly: down 8%. Bonds were 1-2bps wider.

- Merck & Co halted sales of its HPV Vaccine into China. Shares fell 11%. Bonds were up to 7bps wider in longer dates.

- Eurofins had good numbers last week. Performance was concentrated in the ERFFP 0.875 31 which tightened 11bps; the 29s and 30s were almost unchanged.

- McKesson reported strong numbers and growth in higher margin business lines. S&P finally rewarded it with a move to Positive Outlook. An upgrade would put the agency in line with Moody’s and Fitch at Single-A

- Sartorius was the worst performer this week. The bonds have rallied since Mid-January and have now stalled on a cash-price. This week’s underperformance was due to the bund rallying more.

- Bayer agri-chem competitors FMC and Corteva reported well ahead of BAYNGR’s 5th March date. FMC was a disaster with shares down 35%. Corteva fell as much as 7% over 2 days: it reported volume gains but pricing pressure.

- Elsewhere, generally strong numbers for the sector with most of the issuers having reported.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBP: Cable FX Exchange traded Option

Jan-08 13:45

GBPUSD (7th Mar) 124.00p, bought for 2.05, 2.06, 2.07 in ~1.22k.

- This is already ITM, the CME contract also trades close to where the spot is, now at 123.21.

US TSY FUTURES: Post-Weekly Initial/Continuing Jobless Claims React

Jan-08 13:33

- Treasury futures have tempered the post-ADP bounce off lows following softer than expected weekly jobless claims, continuing claims higher w/ prior down-revised.

- The Mar'25 10Y contract trades -2.5 at 108-03 after breaching round number support to 107-28.5 low earlier, 10Y yield currently at 4.7035 +.0185 after tapping 4.7280% high, 2s10s at 42.486 +3.514.

FED: Gov Waller Continues To Forcefully Argue For Cuts, Unconcerned By Tariffs

Jan-08 13:33

Gov Waller's speech (called "Challenges Facing Central Bankers") Wednesday is largely in line with Chair Powell's post-December press conference commentary: further rate cuts are expected if the economy unfolds as expected. But Waller is more forceful on the outlook for cuts than Powell (and apparently more dovish than the median FOMC voter who sees just 50bp of cuts in 2024).

- Waller says: "minimal further progress [on inflation] has led to calls to slow or stop reducing the policy rate. However, I believe that inflation will continue to make progress toward our 2 percent goal over the medium term and that further reductions will be appropriate." Note the "will be". Powell in contrast, albeit speaking for the FOMC as a whole: "we are at or near a point at which it will be appropriate to slow the pace of further adjustments".

- Like Powell, Waller remains confident that inflation is on track to reach 2%: "I believe that inflation will continue to make progress toward our 2% goal over the medium term and that further reductions will be appropriate". He goes through his thinking on inflation trends, including that " progress has been uneven, but disinflation is more apparent if one smooths through the recent upticks" ... and "inflation in 2024 has largely been driven by increases in imputed prices, such as housing services and nonmarket services, which are estimated rather than directly observed and I consider a less reliable guide to the balance of supply and demand across all goods and services in the economy." In other words, no concern from recent inflation data.

- One major takeaway is that Waller doesn't see tariffs as being inflationary ("If, as I expect, tariffs do not have a significant or persistent effect on inflation, they are unlikely to affect my view of appropriate monetary policy.") He doesn't say whether his December forecasts incorporated assumptions of future government policy, but clearly this is the dovish angle on the tariff debate. The December meeting minutes will be interesting to read for any other participants' takes on the tariff impact.

- Unlike Powell, he does not describe his view of the current state of policy restrictiveness: Powell in December said after 100bp of rate cuts that "policy is still meaningfully restrictive"; Waller had said before deciding whether to cut in December that policy was "significantly restrictive".

Related bullets

Related by topic

Credit Sector

Fixed Income

BDX

US

MRK

ERFFP

France

MCK

BAYNGR

Germany

SRTGR