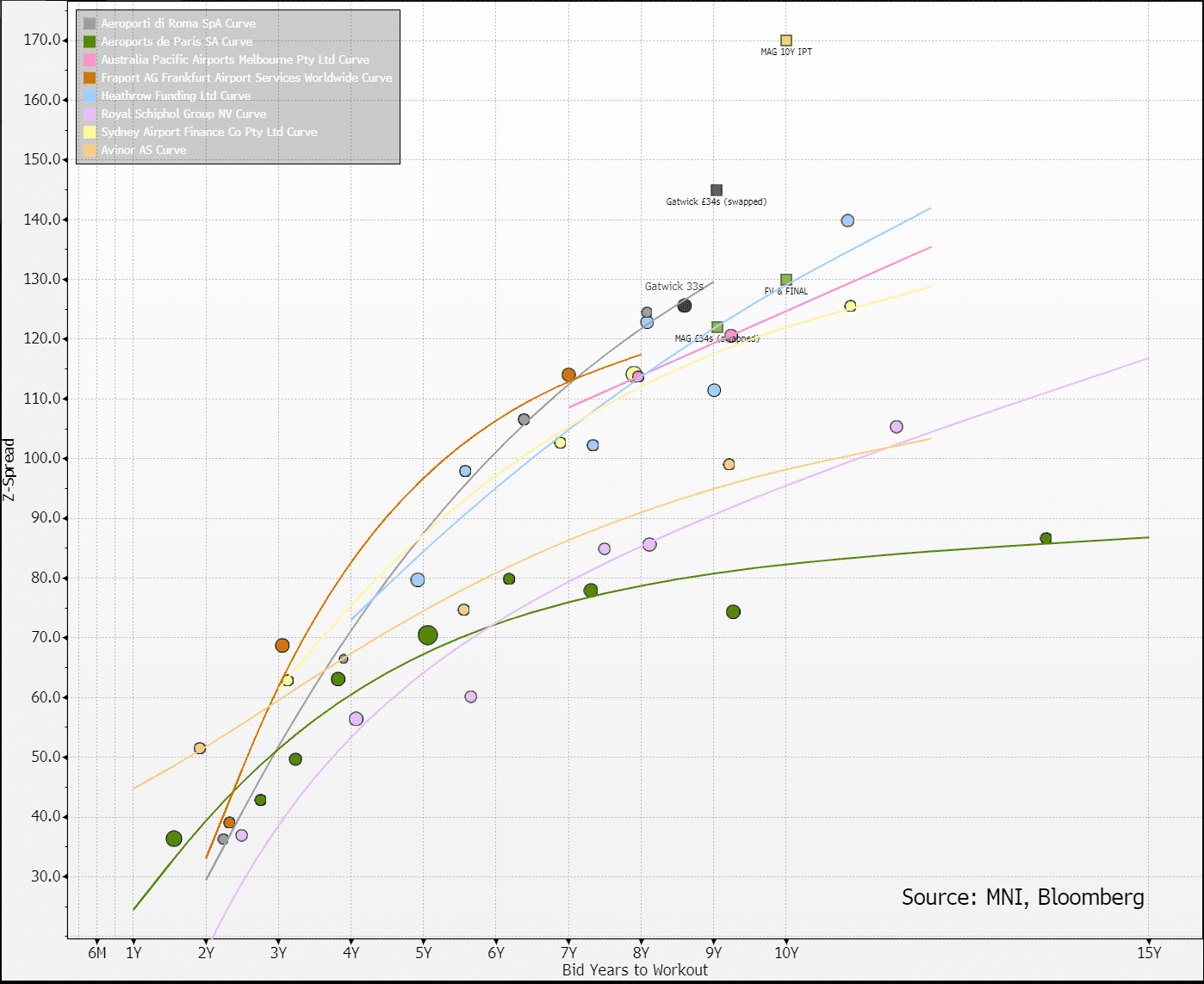

EU TRANSPORTATION: MAG (Stansted & Manchester airport): FINAL

Mar-12 12:03

(MAGAIR 1st lien: Baa1/NR/BBB+: stable)

9.8x cover to welcome it into euros.

- WNG €500m 10Y Snr Sec +130a vs. FV +130 (no NIC)

- -40 in from IPT, books > €4.9b and very firm

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SCANDIS: EURSEK and EURNOK Extend Last Week's Selloffs

Feb-10 11:47

Scandi currencies outperform the G10 basket this morning, with EURNOK and EURSEK each 0.4% lower, extending last week’s selloffs.

- Bearish momentum in EURSEK has been bolstered by a cross of the 50- and 200-day EMAs, with the cross now through Friday’s low and eyeing the Sep 27th low at 11.2450. Speeches from Riksbank’s Seim, Bunge and Jansson headline the remainder of this week’s Swedish calendar.

- NOK strength comes following the higher-than-expected CPI-ATE reading this morning (2.8% Y/Y vs 2.6% cons, 2.7% prior) and the >4.50% rally in European natural gas futures.

- Our Commodities team point to the risk to gas storage from a drop in temperatures and expected boost to heating demand in NW Europe later this week as drivers of today’s TTF rally.

- EURNOK has pierced 11.6000, a notable pivot level going back to mid-2023, which closely coincided with the Dec 4th low (11.5998) and the 61.8% retracement of the June-August '24 rally (11.5953). This exposes the November 25th low at 11.5192 on the downside.

- Tomorrow sees the release of Q4 GDP (consensus and Norges Bank see mainland GDP at 0.3% Q/Q), before Norges Bank Governor Wolden Bache’s annual address on Thursday evening.

EQUITIES: Large Santander Put Option

Feb-10 11:43

BDS2 (17th Apr) 5p, bought for 0.08 and 0.09 in ~29.4k.

US TSYS: Unfazed By Latest Trump Tariffs

Feb-10 11:43

- Treasuries sit mildly twist steeper from Friday’s close, giving a sense of downplaying Trump’s weekend steel and aluminum tariffs announcement.

- That being said, there could still be sensitivity to upcoming details on those tariffs. Today’s docket meanwhile is particularly light although NY Fed inflation expectations take greater prominence than usual considering the partisanship clouding the U.Mich readings.

- Cash yields range from 0.5bp lower (front-end/belly) to 1.5bp higher (30s).

- 2s10s sits at 21.6bp (+0.8bp) vs overnight lows of 19bp but it’s still one of the lowest since mid-to-late December.

- TYH5 has kept to narrow ranges, currently at 109-05+ (-02) on modest cumulative volumes of 305k.

- The short-term trend needle points north, with resistance seen at 110-00 (Feb 7 high, snap reaction to NFP print) before 110-14 (Dec 14 high). To the downside, support at 108-20+ (Feb 4 low).

- Data: NY Fed inflation expectations Jan (1100ET)

- Bill issuance: US Tsy $84B 13W & $72B 26W Bill auctions (1130ET)