POWER: Czech Cez Continues to Up Hedging for 2025-28, Contracted Emissions Rise

Mar-13 09:18

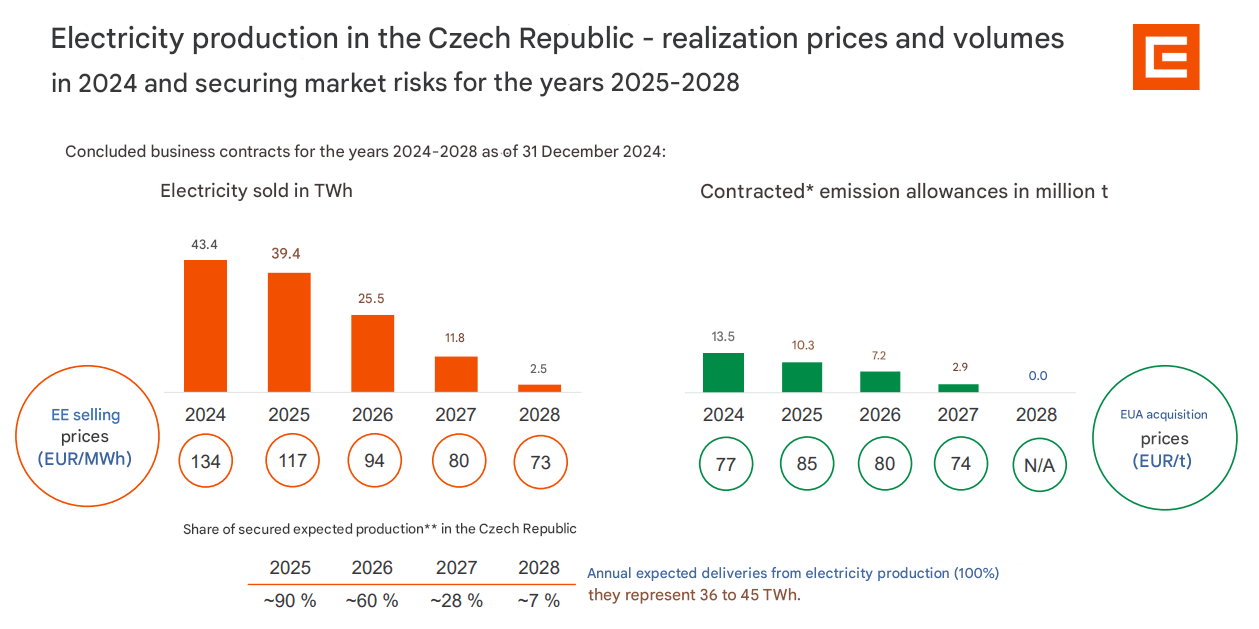

Czech Cez continued to raise its hedging for power delivered in 2025-28 at the end of 2024 from 3Q24, with average prices increasing for 2027-28 delivery. Its contracted emissions rose for all years – except 2028, which still hasn’t been hedged.

- Cez hedged 60% and 28% of its power output for delivery in 2026-27 at an average price of €94/MWh and €80/MWh, respectively at the end of December 2024.

- This is up from the end of September when the firm hedged 49% and 22% of its 2026-27 power at €95/MWh and €79/MWh.

- The firm sold forward 7% of its 2028 power at an average of €73/MWh. This is slightly up from the 5% hedged at the end of 3Q, which was sold at an average of €72/MWh.

- And its hedging for 2025 was at 90% at €117/MWh – climbing from 80% at the end of September 2024 – which was sold at €118/MWh at the time.

- The Czech 2026 baseload power contract settled at €89.29/MWh on 12 March, while the 2027-28 baseload power contracts cleared at €77.92/MWh and €72.42/MWh, respectively on 12 March, according to EEX.

- Additionally, it hedged around 10.3 mn/t of emission allowances for 2025 at an average price of €85/t CO2e at the end of 4Q24, with 7.2 mn/t and 2.9 mn/t of emissions hedged for 2026-27 at an average price of €80/t CO2e and €74/t CO2e, respectively.

- This is up from 9.6 mn/t of emission hedged for 2025 at the end of September 2024, as well as 5.2 mn/t and 1.9 mn/t contracted for 2026-27, respectively. Price falls were evident on the quarter for all years.

The December 25 and December 26 EU ETS contracts are at €69.56/t CO2e and €71.60/t CO2e, respectively, at the time of writing.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOE: Why does Mann think that second-round inflation risks are lower now?

Feb-11 09:18

- On of Mann's main points is that she said last year don't be deceived by headline inflation falling back - and now her message is don't be deceived too much by the upcoming inflation hump ("yet"). This is largely because these moves are being caused by non-domestically driven demand pressures.

- She thinks that the risks of second-round effects are lower now due to:

- Distributions in the wage data - noting that "Expected wage growth is fairly tightly centered around a target-consistent 3% for goods and business-services firms. For consumer-facing firms, currently the greatest probability mass (in aqua) is closer to 4%, which likely is not target-consistent."

- "I judge that the current and likely continued weak demand conditions will lead to a further loosening of the labor market which tend to follow non-linear dynamics. Thus, even if near-term inflation expectations firm on the back of the inflation hump, these factors likely will restrain pass-through to wages and prevent second-round effects from setting in."

- Third on employer NICs: "Those firms who reported reduced employment growth as a margin of adjustment revised down their employment growth expectations significantly (solid versus hollow orange diamonds in Chart 9) following the Budget announcement. Cost increases more generally on firms, particularly smaller ones, expose cash flow vulnerability, with 39% of respondents to the BICS survey holding cash reserves sufficient for less than 4 months. Research suggests that such cash flow vulnerability is associated with job shedding, which may become more apparent as COVID support policies run off.

- On pricing power: "I have focused on the most income and price elastic categories of products as the leading indicators of how consumer behavior can discipline firms’ pricing strategies. In the latest disaggregated data, the decelerations in these categories such as catering, culture, and hospitality have become more systematic."

- "Looking beyond 2025, I judge that the dynamics of soft sales volumes, already observed for a year, will be accentuated as household savings rates remain high, both as an ongoing precaution against volatility in purchasing power and then also on account of heightened unemployment concerns. This likely soft consumption profile will constrain firms’ pricing power and will moderate pass-through of costs."

FOREX: FX OPTION EXPIRY

Feb-11 09:16

Of note:

EURUSD 3.83bn at 1.0300/1.0330.

USDJPY 1.03bn at 152.00.

EURUSD 1.78bn at 1.0300 (wed).

AUDUSD 1.04bn at 0.6200 (wed).

EURUSD 1.63bn at 1.0300 (fri).

USDJPY 2.3bn at 152.00 (fri).

AUDUSD 1.17bn at 0.6200 or ~1bn at 0.6300 (fri).

USDCNY 2.16bn at 7.3000 (fri).

- EURUSD: 1.0250 (545mln), 1.0275 (903mln), 1.0300 (1.29bn), 1.0305 (459mln), 1.0320 (1.33bn), 1.0325 (271mln), 1.0330 (479mln), 1.0375 (583mln).

- USDJPY: 152.00 (1.03bn).

- USDCAD: 1.4355 (460mln).

GILT SYNDICATION: New 10-year: 4.50% Mar-35 gilt: Spread set

Feb-11 09:15

- Spread set at 4.25% Jul-34 gilt + 5.5bp (guidance was + 5.5/6.0bps)

- Size: GBP benchmark (MNI expects GBP8.5-10.0bln)

- Orderbooks in excess of GBP110bln (inc JLM interest of GBP9.6bln)

- Maturity: 7 March 2035

- ISIN: GB00BT7J0027

- Settlement: 12 February, 2025 (T+1)

- Bookrunners: Barclays, BNP Paribas, Citi (B&D/DM), Goldman Sachs International Bank, HSBC and NatWest.

- Timing: Books to close at 9:30GMT, pricing later today

From market source