EU CONSUMER STAPLES: Consumer & Transport: Week in Review

After waiting for more than half-a-year Carlsberg supply finally arrived – the first M&A deal in consumer this year. Seems secondary had learnt from DSV mistakes, staying within peers and not far off final pricing. Primary stayed interesting on Kraft and Edenred, both pricing -5 through our FV’s and echoing secondary that was keen for another week of blatant compression. It will be a topical week in earnings on Auchan in HY and Adecco in IG.

- FDJ issues prelim FY results that are firm but flags an HSD headwind to earnings next year on French tax increases. On the low levered balance sheet and otherwise firm growth it is not a mover.

- Edenred results show a noticeable slow-down in Europe. Guidance remains unchanged but equity analyst are starting to question if it can hit the numbers. We have become less enthused since the Italy regulation had an outsized impact on earnings, particularly in the face of ongoing regulatory discussions in France. Elevated equity payouts are having little impact on the share price that is trading on a multiple well below typical growth stocks.

- Finnair: revisit to FY results from last week that remained lacklustre, but stable. It faces near term negative catalyst on ongoing pilot strike impacts. It may still be an attractive name for carry investors on positive governance and the government ownership/uplift.

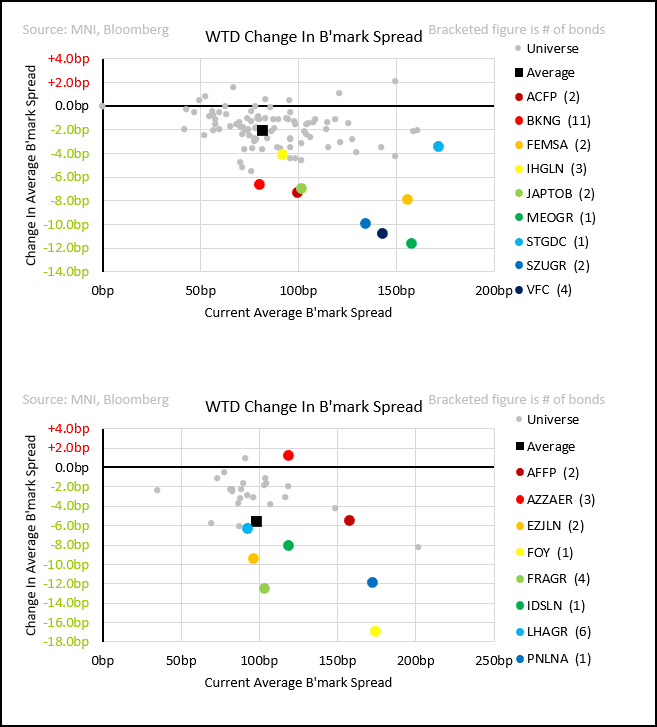

Event-driven movers

- Auchan: no-end to earnings drama with a local paper leaking detailed numbers a week before scheduled earnings. The leaks have some bad and good details – the lack of near term positive catalyst and still weak macro from peers will leave net encouraging caution if they are accurate.

- PostNL requests direct financial support from the Dutch government. Reuters quoting the ministry’s response, indicates financial support will not be coming. PostNL has generally only asked for changes to delivery requirements, 40% drop in operating profit may be motivating it to ask for more.

- Campari will cut 10% of its workforce according to a local papers. It was guiding to reducing SG&A so we are not too concerned. Equities +5% on the week.

- Barry Callebaut: is in dispute with local exporting group who want more than the regulated price according to Bloomberg. Barry will not be able to buy above it and local exporters generally make up a small percentage of total exports.

- Lufthansa some caution from us on the strong retail bid vs fundamentals gap – one that is opening up rotations with spread pick-up to firmer names. Headlines later in the week indicate it may acquire Munich airport ground services operator, likely to streamline current inefficiencies – size unlikely to be credit mover.

- Haleon is being given the cold-shoulder in sterling markets sending the spread against Reckitt in the opposite direction to what we would expect. The sterling 33s may screen value to investors.

Primary

- Carlsberg 2y FRN / 4.5y (+3) / 7y (+1) / 10y (-2) / £14y (-4). Kraft Heinz: 8y +97 (-5), Edenred 5.5y (-5)

Rating action

- Walgreen Boots (unsec; B1 Neg now/ BB- Stable); Moody’s moves to negative outlook still seeing a recovery ahead but with more uncertainty in the face of ongoing legal disputes, weak consumer environment and reimbursement pressure.

- Carnival (unsec; B1 Pos now/BB pos/BB Pos); Moody’s with 1-notch upgrade and stays on positive outlook. It continues to notch unsecured (including local lines) aggressively below the secured.

- British American Tobacco (Baa1/BBB+); S&P with a sanguine take on what we saw as lacklustre and weaker than peer FY earnings flagging “good rating headroom” on leverage.

- Nestle (Aa3/AA-; Stable); S&P flags little headroom to double-A ratings. Co’s stated leverage target is indicative it will hold onto it.

- Allywn (NR/BB/BB- Pos); Fitch moves to positive outlook

- Aeroports de Paris (NR/A-/BBB+; Stable); S&P follows FY results saying it expects comfortable rating headroom to remain - even in the face of higher income taxes and increase in solidary tax on airfares.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Trump Comments on Venezuelan Oil Sees as Negotiating Tactic: Platts

President Donald Trump's suggestion that the US will "probably" stop buying oil from Venezuela is seen as a negotiating tactic rather than policy, Platts said.

- David Goldwyn, president of Goldwyn Global Strategies and chair of the Atlantic Council Global Energy Center's Energy Advisory Group, believes Trump is increasing pressure on Venezuela ahead of negotiations.

- Goldwyn argued that Trump's "America First" policy aims to reduce migration pressure, avoid reintroducing certain countries to Venezuelan oil control, moderate US energy prices, and prevent a humanitarian crisis.

- Trump advisors told Axios earlier in the week that the administration wants regime change in Venezuela but that “doesn't necessarily mean military action.”

- Experts are divided on whether Trump will revoke US licenses for oil companies operating in Venezuela.

- Ryan Berg, director of the Americas Program at the Center for Strategic and International Studies, suggested licenses might be reversed but it won’t necessarily lead to the return of "maximum pressure".

- However, replacing Venezuelan crude would be complex as local US grades are misaligned with refinery needs.

MNI EXCLUSIVE: MNI Talks To EU Officials

EU officials are scrambling for ways to face up to the economic challenge of the U.S. under Trump.-On MNI Policy MainWire now, for more details please contact sales@marketnews.com

GILT AUCTION PREVIEW: On offer next week

The DMO has announced it will be looking to sell GBP3bln of the 0.875% Jul-33 Green Gilt (ISIN: GB00BM8Z2S21) at its auction next Wednesday, January 29.