POWER: French Hydro Stocks Resume Trend Lower

Mar-31 15:49

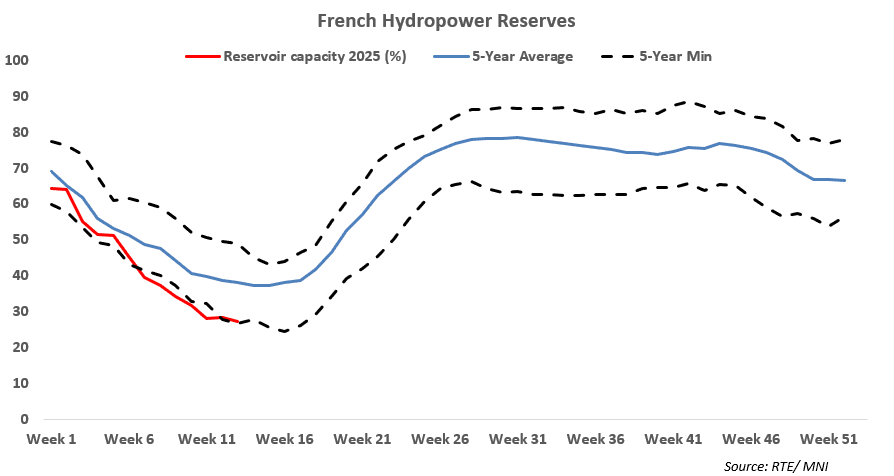

French hydropower reserves last week – calendar week 13 – resumed the decline, after rising the week prior, to 27.3% of capacity, down from 28.3% the week before, RTE data showed.

- The weekly increase was due to low precipitation, slightly higher hydropower generation and a sharp decline in wind generation. Stocks edged up by 0.24 percentage points the week prior.

- The deficit to the five-year average widened to 10.8 points, from 10.3 points the week before.

- The deficit to 2024 levels was broadly stable at around 8 percentage points.

- Power demand in France decreased further to 51.75GW last week, down from 53.02GW the week before.

- French nuclear generation last week increased by 824MW to 42.06GW.

- Hydropower output from reservoirs last week edged up by 135MW to 1.79GW. Output from pumped storage also edged up by 157MW to 1.07GW. Run-of-river generation last week inched up by 143MW to 4.35GW.

- Wind output in France last week declined by 3.07GW to 4.09GW, while solar PV output rose by 275MW to 3.72GW.

- Precipitation in the hydro-intensive region of Grenoble last week totalled 3.8mm, compared with the seasonal normal of 18.5mm.

- Looking ahead, the latest weather forecast for Grenoble for this week suggests little precipitation, limiting inflows into reserves.

- The latest ECMWF weather forecast for Paris for this week suggests mean temperatures between 9.4C and 15.3C.

- French nuclear generation capacity is forecast to average 46.36GW – which would be up on the week – according to Reuters.

- Nuclear availability in France stood at 72% of capacity as of 31 March, RTE data showed, cited by Bloomberg.

Wind output in France for the remainder of this week (Tues-Sun) is forecast to be high at 5.39GW to 12.19GW during base load according to SpotRenewables.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: A Stacked Week Ahead For US Macro

Feb-28 21:45

- Next week sees a series a key risk points, starting with trade policy and Trump’s Mar 4 deadline for an additional 10% tariffs on China (for 20% total) and the imposition of the delayed 25% tariffs on Canada and Mexico. US Treasury Sec Bessent offered a potential offramp here, saying Friday afternoon the US wants to see Canada and Mexico match tariffs on China. Whilst following through with that could see temporary de-escalation in US trade tensions with Canada and Mexico, it would likely stoke greater likelihood of China retaliation and/or further fiscal support.

- It’s bookended by ISM manufacturing (Mon) and services (Wed) reports, watched to see whether sharp increases in manufacturing prices paid seen in other surveys first show up in this broader measure and whether there is sign of spillover to services.

- The main data release of the week comes on Friday though, with the nonfarm payrolls report for February.

- The January report saw a modest miss for nonfarm payrolls but it was more than offset by a robust two-month net revision along with a smaller than expected benchmark revision. Further, the unemployment rate again surprised lower at 4.0% for its lowest since May 2024 in a further step away from the 4.3% the median FOMC member forecast for 4Q25 in the December SEP.

- Early days for the Bloomberg survey see nonfarm payrolls growth at a seasonally adjusted 155k in February and for the unemployment rate to hold at that lower 4.0%.

- Note that the nature of the DOGE “deferred resignation program”, with some 77k federal employees accepting the offer, shouldn’t see any direct impact on payrolls growth (in the establishment survey) until the October report as workers will remain on the payroll in the interim. One area where the direct impact could show however is the household survey. Assuming those who accepted the offer are treated as equivalent to a furloughed worker, they’ll register as unemployed. A word of caution though, it’s a much more volatile survey, with a 90% confidence level of +-600k for employment vs +-136k for payrolls.

- Note that post-payrolls Fedspeak sees a notable addition this time, with Fed Chair Powell set to talk on the economic outlook with both text and Q&A, starting at 1230ET. Data and tariff deliberations should still set the tone, but at this juncture we wouldn’t be surprised to see a continued call for patience in rate cut expectations considering dovish repricing seen over the past week. This is a theme that could be seen from other notable Fedspeakers throughout the week, including permanent voters Williams, Waller and Kugler.

STIR: Significant Dovish Repricing In US Rates This Week

Feb-28 21:14

- The softer growth outlook has dominated signs of renewed inflationary pressures this week - see a key summary of the week's macro developments in the MNI US Macro Weekly here.

- Fed Funds futures have a next 25bp Fed cut now fully priced for June and over the week have added nearly an entire 25bp cut over 2025 with a cumulative 70bp of cuts vs the 50bp implied by the median FOMC dot in Dec.

Significant dovish adjustment over the week:

MACRO ANALYSIS: MNI US Macro Weekly: No Escaping Tariff Distortions

Feb-28 21:12

- We have published and e-mailed to subscribers the MNI US Macro Weekly offering succinct MNI analysis across the range of macro developments over the past week.

- Please find the full report here: https://media.marketnews.com/US_macro_weekly_250228_3f0cf485bb.pdf