EU HEALTHCARE: Healthcare: Week in Review

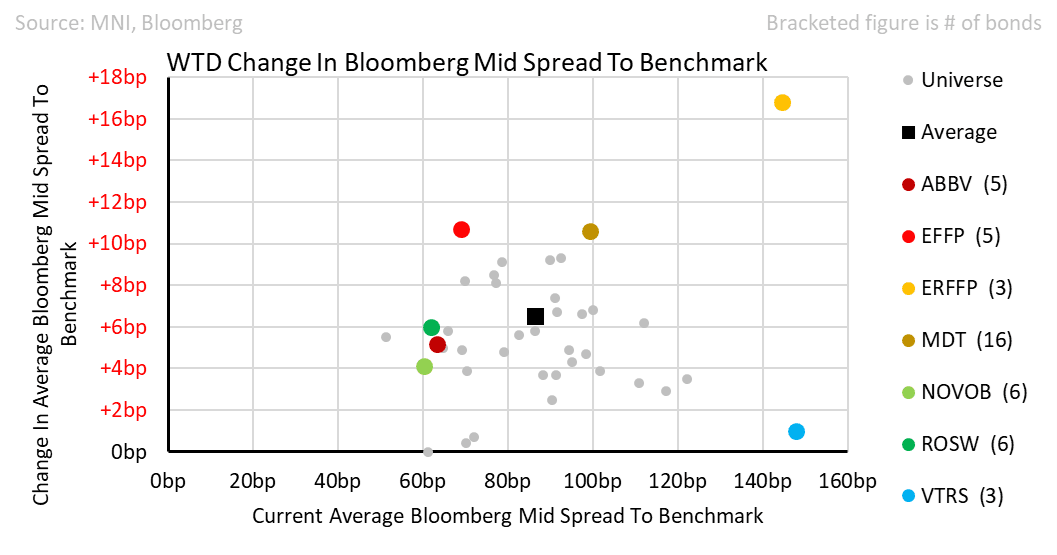

The whole market had a challenging week and Healthcare was no different. Spreads on average were +6bps wider vs Bunds. Eurofins was the worst performer as higher beta names suffered, despite last week’s Fitch affirmation. Viatris, however, found some stability after a +35bps widening in 3 weeks.

• Galderma brought an inaugural €500 5yr at DBR +112.2 Thursday was a particularly weak day in the markets and this deal was quoted around 5bps wider. GALDSW equity is off the highs, but the stock market still places a high value on the growth potential of the company with consumer aesthetics warranting a higher multiple than pharma. The company is guiding for further leverage reduction from 2.3x to <2.0x One to watch.

• Viatris found some relief on Monday as Fitch affirmed its BBB Stable rating, in contrast to S&P’s recent cut to BB+. Fitch acknowledge the revenue reduction from the FDA actions concerning Indore but view this as a temporary setback.

• Novo Nordisk was +4 wider. The market cap is now 50% of last June as competition in the weight-loss space increases. Roche signed a deal with Zealand pharma to develop an amylin analog. This saw ROSW pay $1.65bn upfront and potentially $5.3bn over time as milestones are reached. Last week, AbbVie struck a deal for amylin with Gubra for a smaller sum. Amylin can be seen either as complimentary to GLP1 or as a more tolerable alternative

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: SOFR Option Update: Puts Pick-Up Pre-CPI

- 4,000 0QJ5 95.43/95.50 2x1 put spds ref 96.03

- 10,000 SFRZ5 95.37/95.50 put spds ref 95.975 to -.97

- 2,000 0QG5 95.81/95.93/96.06 put flys ref 96.01

EURIBOR OPTIONS: Call condor seller

ERM5 97.875/98.00/98.0625/98.1875c condor, sold at 3.5 in 10k.

EURIBOR OPTIONS: Call spread vs call

ERU5 98.12/9837cs vs ERM5 98.0625c, bought the cs for 3.25 in 5k.