EU CONSUMER CYCLICALS: Kering | 1Q results (x5)

Apr-24 17:42

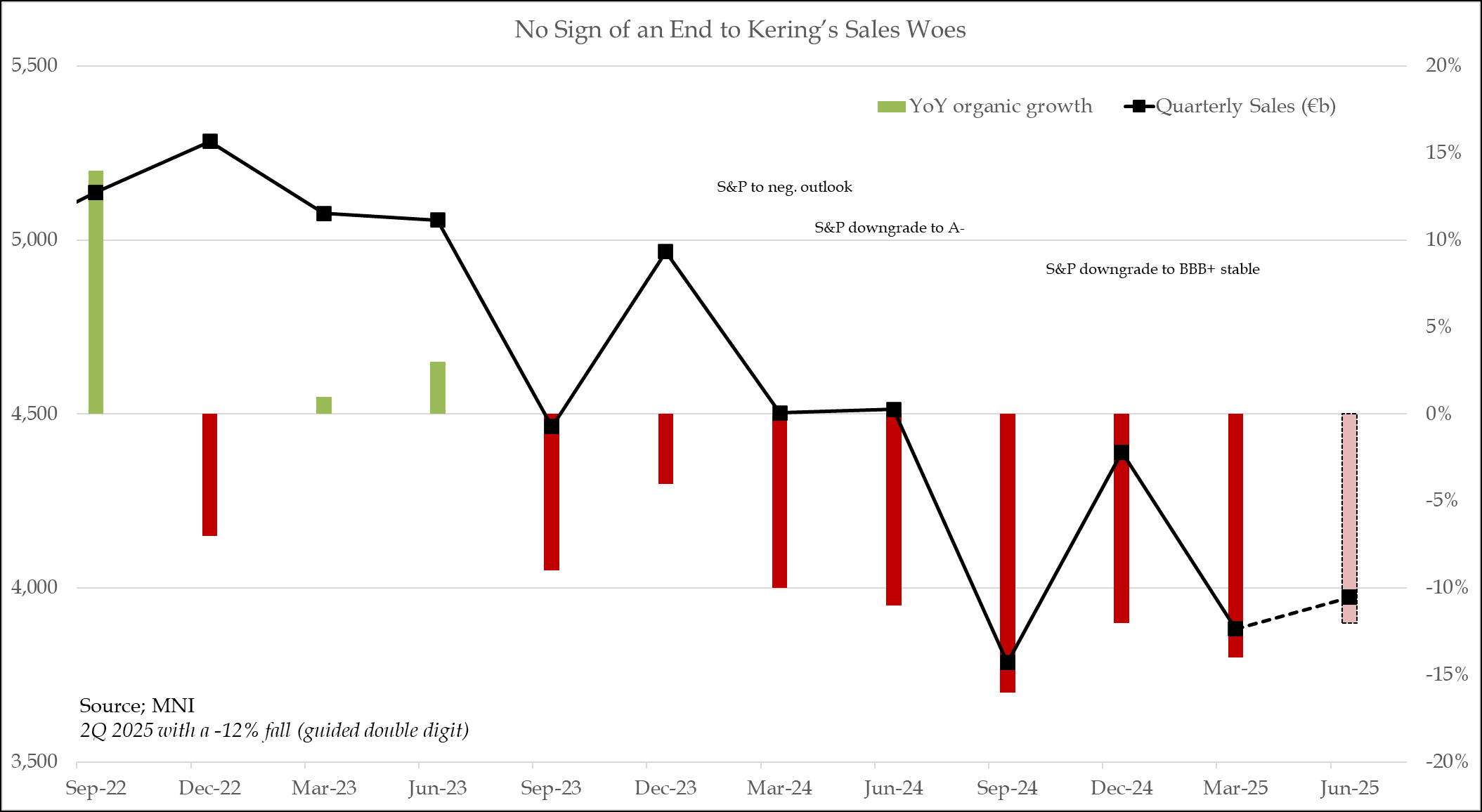

(KERFP; NR/BBB+ Stable)

So it's clear our view is;

- S&P will move to a negative outlook as leverage trends beyond the BBB+ threshold this year

- A downgrade may be avoided as the company is guiding to ~€2bn in non-core real estate disposals over the next two years (potential for ~0.5x leverage relief)

- We do not see it as attractive enough on RV to step in now — effective guidance points to a ~37% fall in 1H EBIT (to be reported 29 July), and performing non-lux BBB retailers offer ample spread pickup

- There were no signs of stabilisation in 1Q earnings or April trading conditions

- It's unclear what happens if the group can’t fix its issues — the company is majority family-controlled (in voting power), reducing the likelihood of a takeover or meaningful management change

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Florida Special Election To Provide Temperature Check On Electorate

Mar-25 17:23

An April 1st special election in White House National Security Advisor Mike Waltz’s former seat in Florida’s 6th Congressional District will provide the first hard data on the mood in the electorate since President Donald Trump took offic.

- Waltz won the district by 33 points in November, but a recent funding disparity between the Republican candidate Randy Fine and Democrat Josh Weil, who has brought in over USD$10 million has raised alarm bells in GOP HQ.

- Punchbowl reports. “Democrats tell us they aren’t expecting to come close to flipping the seat blue… But if Weil keeps Fine’s expected victory to the low double digits, then the party can credibly claim a groundswell of support in an ultra-conservative seat.”

- Punchbowl adds: “The real fear for Republicans is that a large Democratic overperformance in the 6th District will fuel liberal narratives that 2026 is gearing up to be a big, 2018-style wave election. Democrats used anti-Trump fervor that year to win more than 40 seats and seize control of the House.”

- House Minority Leader Hakeem Jeffries (D-NY) said: “These are races that should not, under ordinary circumstances, be on anyone’s political radar. They are safe Republican seats that Donald Trump won by more than 30 points. The American people are not buying what the Republicans are selling.”

ECB: Villeroy Maintains Dovish Tone, Questions Fiscal Inflation Impulse

Mar-25 17:10

Typically dovish comments from Villeroy in an interview with Germany’s Faz. The language around the inflation impact from tariffs is similar to comments from last week but he goes into a little more detail on potential fiscal impacts here:

- "*ECB'S VILLEROY: EASING CYCLE NEITHER FINISHED NOR AUTOMATIC

- *VILLEROY: ECB STILL HAS SCOPE TO EASE POLICY

- *VILLEROY: MARKET VIEW OF 2% RATE IN SUMMER IS POSSIBLE SCENARIO

- *VILLEROY: PACE AND EXTENT OF ECB EASING REMAIN OPEN" - bbg

- “*VILLEROY: GERMANY'S FISCAL PLAN DOESN'T NECESSARILY FUEL PRICES

- *VILLEROY: NO SIGNIFICANT INFLATION EFFECT IN EU FROM TARIFFS” - bbg

- “The German program is a historical game-changer for Germany and for Europe. However, in order for the program to be a complete success, the supply, the capacity to produce, must increase as much as the funding.”

BUNDS: Markets Wary Of Non-Monetary Policy Driven Bund Downside

Mar-25 17:10

- Despite the today’s net downtick, Bunds continue to print well above their lows seen during the aftermath of the German fiscal announcement on March 4. RXM5 is currently ~160 ticks higher, whilst in cash space, the 10Y currently trades around the 2.8% handle vs highs of almost 2.94% although it still compares with sub 2.5% prior to the announcement.

- Markets appear wary of further downside for the contract: The difference between a June expiry Bund future 25 delta put and the respective call contract continues to print in positive territory, having pared around half of its initial spike following the March 4 announcement. This mirrors our Europe Pi published yesterday, which sees Bund positioning as very short.

- Tellingly, this is counter to the volatility skew in 3m Euribor futures, which has seen no material shift since early March, with 25 delta puts for the Jun’25 continuing to be modestly more expensive than respective calls. This would suggest that Bund wariness appears not to be driven by European STIR, or, said differently, market pricing appears expensive for hedging against further ASW tightening.

- From a fiscal risk angle, tomorrow will see a constitutional court judgement on the so-called solidarity surcharge in Germany - if the case is upheld, it would directionally favour short Bund positioning vs Swaps. See an overview of the case and potential implications here.

- However, leaving aside this singular event, from a fundamental perspective, already short positioning, the lack of an immediate ramp up in issuance and lingering tariff threats present some clear risks against further ASW tightening in the near term.