EM CEEMEA CREDIT: MNI EM Credit Market Wrap - CEEMEA (14 Feb)

| MNI EM Credit Market Wrap - CEEMEA (14 Feb) |

U.S. Treasuries were relatively flat for most of the day, but the weak US retail economic figures resulted in 10Y -7bps @ 4.47%, and the 5s/10s +1bps @ 14.55. Emirates NBD hosted a roadshow for investors on their USD benchmark PNC6 which we expect will be launched Monday. We think more deals could come to the market next week as the pipeline looks relatively healthy.

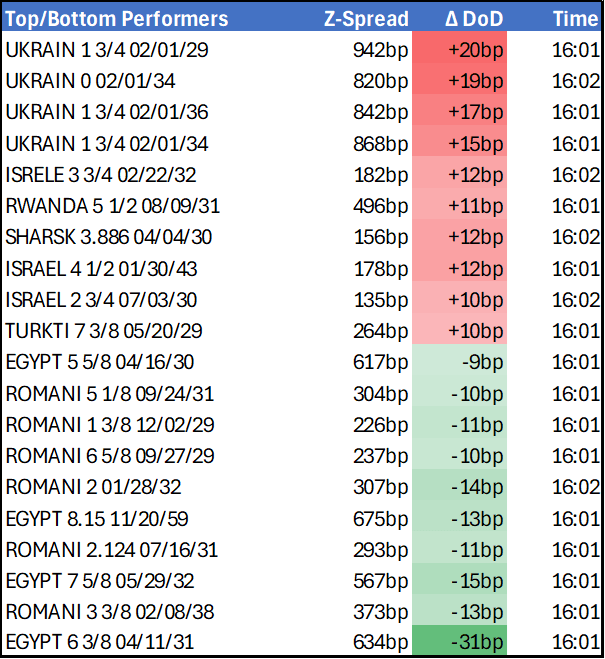

In secondary, Romani bonds were tighter across the curve following the central bank’s decision to keep interest rates unchanged. EGYPT bonds were tighter across the curve on limited news flow and the 10Y bonds -7bps. UKRAIN bonds continue to be in focus with the Munich security conference underway, the curve was wider and the 1.75% Dec35 benchmark bonds +11bps. Corporate news flow was limited to Tabreed’s FY 24 earnings, which were broadly inline with expectations and supportive for spreads in our opinion. Metiinvest also reported production figures, but a potential Ukraine peace deal will be the key for bonds.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: EURUSD Reverses Post-CPI Move, EURJPY Down 1.05%

- The US dollar has been gradually paring losses in recent trade, with the greenback assisted by equities moderately off their best levels. EURUSD stands out, having entirely reversed the post-CPI move to trade back at 1.0300. Notably, the single currency underperformance keeps EURGBP on the backfoot, edging closer back to 0.8400, while EURJPY extends session declines to over 1%. Below here for EURJPY, the focus will be on 160.00, a notable pivot for the cross, coinciding with the Monday low.

US INFLATION: Core PCE Estimates Tilt Lower After CPI Report

Some post-CPI core PCE estimates below - while not all had pre-CPI/PPI forecasts, it's pretty clear that CPI points to a slightly softer figure than seen coming into this week and certainly after PPI (pre-PPI it was around 0.20%, post-PPI it looked to be closer to 0.25%, now looks to be back to 0.20% or the high 0.10s%).

December Core PCE % M/M ests (0.11% prior):

- Wells Fargo 0.21%

- Nomura: 0.205% (had been 0.272% pre-CPI, post-PPI)

- HSBC: 0.2% (rounded)

- Cleveland Fed nowcast: 0.189% (had been 0.23% pre-PPI and pre-CPI)

- JPM 0.186%

- Morgan Stanley: 0.166%

US-RUSSIA: Treasury Announces New Measures On Russia To Curb Sanctions Evasion

The US Treasury Department has announced a raft of new sanctions on financial institutions determined to aid Russia in evading US-led sanctions or supporting Russia's military-industrial base.

- The measures are part of a major push by the Biden administration to harden rules against Russia and China before President-elect Donald Trump takes office next week. Other measures announced include strict sanctions on Russia's energy sector and an expansion of export controls on semiconductors related to AI to China.

- A Treasury statement notes: "This action targets a sanctions evasion scheme established between actors in Russia and the People’s Republic of China (PRC) to facilitate cross-border payments for sensitive goods."

- The statement adds: "Today’s sanctions also include dozens of companies across multiple countries that continue to support Russia’s efforts to evade U.S. sanctions, particularly in the PRC, which remains the largest supplier of dual use items and enabler of sanctions evasion in support of Russia’s war effort."

- Deputy Treasury Secretary Wally Adeyemo said in a statement: “Today’s actions frustrate the Kremlin’s ability to circumvent our sanctions and get access to the goods they need to build weapons for their war of choice in Ukraine. Today’s expansion of mandatory secondary sanctions will reduce Russia’s access to revenue and goods.”

- The Treasury Dept notes: "...foreign financial institutions that conduct or facilitate significant transactions or provide any service involving Russia’s military-industrial base... run the risk of being sanctioned by [Office of Foreign Assets Control]."