MNI EUROPEAN MARKETS ANALYSIS: Equity Sentiment Up, USD Down

- Equity sentiment has been better in Asia Pac markets, while US futures are higher, led by tech. Carry over from tariff reprieves for key tech products (released late on Friday) has aided sentiment. Still, US President Trump stated that semiconductor tariffs were coming soon.

- US Tsy yields have consolidated after last week's sharp spike. The USD remains on the backfoot against most of the majors, with JPY and NZD gains evident. The exception remains the CNH.

- It's a quiet start to the week in terms of the EU data calendar. In the US we have NY Fed inflation expectations.

MARKETS

US TSYS: Richer After Last Week's Sell-Off

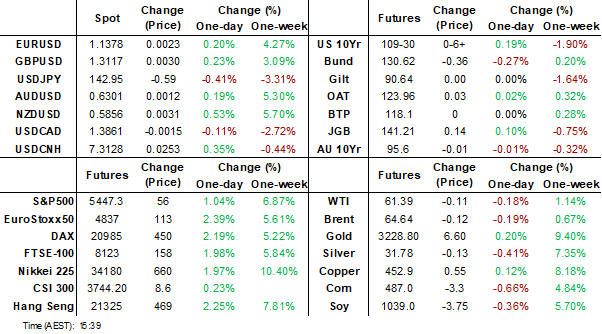

TYM5 has traded in a tight 109-17/109-31 range, going into the London open trading near its highs around 109-31,+0-07+ from its close on Friday.

- The 10-year yield has consolidated in a tight range of 4.4561 - 4.4876 in Asia.

- The market is starting to realise the FED will not be stepping in to rescue it by cutting rates, as long as it expects inflation to track higher on the back of Trump’s policies.

- This will be a big week for US tsys but it feels there has been some trust lost and there is more position unwind to come. Dips back towards 4.25/30% should now find supply, with the bigger 4.80/5.00% area now being targeted.

- Any move back to 5% and above would start to become problematic for equities.

- Data/Events: Powell and Waller to speak on Wednesday, Retail Sales 16/04

JGBS: Sharp Bear-Steepener Ahead Of Tomorrow's 20Y Supply

JGB futures are stronger, +8 compared to the settlement levels, sitting near the middle of today’s range.

- In the final report, Feb. industrial production was revised down to 2.3% m/m from 2.5%. Japan’s operating ratio fell to 104.1 in Feb. compared to 105.3 in the previous month.

- (MNI) The BoJ will manage monetary policy appropriately to achieve the 2% price target sustainably and stably, Governor Kazuo Ueda told lawmakers Monday. The BoJ will examine the future economy, prices and financial markets without precondition, he added.

- Cash US tsys are 2-3bps richer in today's Asia-Pac session. The US calendar is light this week, with the highlights being Retail Sales data and Fedspeak from Powell and Waller on Wednesday.

- Cash JGBs are flat to 11bps cheaper across benchmarks, with a steepener curve. The benchmark 20-year yield is 7.9bps higher at 2.407% ahead of tomorrow's supply. The current yield is 10-15bps higher than last month’s auction level.

- The swap curve has twist-steepened, with rates 2bps lower to 5bps higher. Swap spreads are mixed.

- Tomorrow, the local calendar will be empty apart from 20-year supply.

AUSSIE BONDS: Bear-Steepener But Well Off Cheaps, RBA Minutes (April) Tomorrow

ACGBs (YM -6.0 & XM flat) are cheaper but sit well above Sydney session cheaps.

- With the local calendar light today, cash US tsys have proved to be the key driver of today’s local market fluctuations. Cash US tsys are 2-3bps richer, with a steepening bias, in today's Asia-Pac session after Friday's heavy session.

- Last week, the US 10-year yield rose almost 50bps in 5 days, one of the biggest moves in that number of days since 1998. The US calendar is light this week, with the highlights being Retail Sales data and Fedspeak from Powell and Waller on Wednesday.

- Cash ACGBs are flat to 6bps cheaper with the AU-US 10-year yield differential at -7bps.

- Swap rates are 2bps lower to 6bps higher, with the 3s10s curve steeper.

- The bills strip has bear-steepened, with pricing -2 to -7.

- RBA-dated OIS pricing is 2-11bps firmer across meetings today. A 50bp rate cut in May is given a 39% probability, with a cumulative 118bps of easing priced by year-end (based on an effective cash rate of 4.09%).

- Tomorrow, the local calendar will see the release of the RBA Minutes for the April Meeting.

- The AOFM plans to sell A$1000mn of the 3.50% 21 December 2034 bond on Wednesday.

BONDS: NZGBS: Closed Near Yield Lows, Curve Twist-Flattened

NZGBs closed showing a twist-flattener, with benchmark yields 4bps higher to 3bps lower. Nevertheless, all NZGB yields closed well off session highs after weaker-than-expected card spending data.

- Cash US tsys also assisted the move away from session yield highs. Cash US tsys are 2-3bps richer, with a steepening bias, in today's Asia-Pac session after Friday's heavy session.

- Last week, the US 10-year yield rose almost 50bps in 5 days, one of the biggest moves in that number of days since 1998. The US calendar is light this week, with the highlights being Retail Sales data and Fedspeak from Powell and Waller on Wednesday.

- Swaps closed mixed, with rates 3bps higher to 1bp lower. The 2s10s curve closed flatter.

- RBNZ dated OIS pricing closed 1-6bps firmer across meetings. 31ps of easing is priced for May, with a cumulative 79bps by November 2025.

- Tomorrow, the local calendar will see Food Prices and a speech from the RBNZ’s Chief Economist About Forecasting.

- On Thursday, the NZ Treasury plans to sell NZ$275mn of the 3.00% Apr-29 bond and NZ$225mn of the 4.25% May-36 bond.

FOREX: Antipodean Wrap - AUD & NZD Holding Onto Gains

The AUD and NZD have both held onto their respective gains from last week in tight Asian ranges. Broad USD weakness last week has seen an overhang of AUD and NZD shorts being pared back.

- AUD/USD - Asian range 0.6278 - 0.6314, AUD has traded sideways for the whole Asian session, albeit near the highs of last week. Shorts will be hoping for sellers to return but will be watching the 0.6400 area this week for signs of breaking to signal the next leg of position squaring.

- AUD/JPY - Asian range 89.57 - 90.81, AUD/JPY fell away early in the session moving down to the 89.60 area before buyers reemerged. Price goes into the London open around 90.00. AUD/JPY is trying to build a base as risk stabilises, but it remains to be seen if this will last. Expect supply once more back towards the pivotal 94.00 area.

- NZDUSD - Asian range 0.5819 - 0.5860, NZD has traded sideways the whole session but there is still no dip. NZD printing around 0.5850 going into London, the market is short and the price action poor. Watch a close above the 0.5850 area for the next potential level to trigger short covering.

- AUD/NZD - Asian range 1.0754 - 1.0830, the cross drifted lower in the Asian session before finding some buyers towards the 1.0760 area. The cross is going into London pretty directionless but the risk still feels that bounces will be capped as liquidity in the NZD dries up quicker than for the AUD on any move higher.

Fig 1: NZD Spot

Source: MNI - Market News/Bloomberg Antipodean Wrap - AUD & NZD Holding Onto Gains

FOREX: USD Bear Cycle Continues

Broad USD weakness over the course of last week as a rotation out of US assets seems to be gathering momentum. The BBDXY is down -0.18% in Asia today. The European Union is racing to clinch trade deals with countries around the globe in an effort to diversify away from an increasingly protectionist US.

- EUR/USD - Asian range 1.1318 - 1.1409, dipped initially on the early Monday open but has since traded bid to go into the London open around 1.1375. EUR/USD had been trading very closely with the 10 year rate differential, this relationship broke down completely last week. The market will be watching to see if this continues this week.

- GBP/USD - Asian range 1.3064 - 1.3128, trading just off the day's highs going into the London session.

- USD/CNH - Asian range 7.2786 - 7.3173, the USD/CNY fix was another higher one at 7.2110, this has seen USD/CNH bounce strongly from the 7.2800 area. USD/CNH goes into the London open near the session highs.

- USD/JPY - Asian range 142.25 - 144.06, was under pressure from the open once again. Falling back to last week's lows around 142.00 into the Japanese fix. It seems any paring back of positions done on Friday going into the weekend have quickly been re-established. Huge support level around 140, a break here could see the move accelerate.

- Cross asset : SP +1.02%, Gold 3230.00, US 10yr 4.46%, BBDXY 1232, Crude oil 61.20.

ASIA STOCKS: A Better Day on Tariff Pause Headlines.

Asia’s major bourses had a better day after President Trump paused import duties on consumer electronics giving a boost to investor sentiment across the region. Whilst the pause is temporary, it gives markets time to pause and focus on other areas in the global economy where risks are rising.

- In China the Hang Seng led the way today rising +2.4%, with the CSI 300 up +0.47%, Shanghai up +0.86% and Shenzhen up +1.5%.

- The Kospi had a solid day rising +0.91% in a week where the Central Bank meets.

- In Malaysia, the FTSE Malay KLCI is up +1.4% in a week where 1Q GDP is released.

- For Indonesia, the Jakarta Composite is putting in another day of solid gains rising +2.00% following stronger than expected FX Reserve data.

- In Singapore, the MAS eased policy and pointed to lower growth whilst the FTSE Straits Times rose +1.46%.

- India’s NIFTY 50 is very strong this morning, rising +1.9% ahead of this week’s CPI release where it is expected that inflation will continue to moderate.

ASIA STOCKS: Outflows Continue Despite Inflow for Taiwan

Relatively constant outflows mixed with the odd meaningful inflow continues to be the thematic we see as we watch the equity flows across the major markets.

- South Korea: Recorded outflows of -$467m as of Friday, bringing the 5-day total to -$2,948m. 2025 to date flows are -$11,478, m. The 5-day average is -$590m, the 20-day average is -$296m and the 100-day average of -$152m.

- Taiwan: Had inflows of +$1,022m as of Friday, with total inflows of +$530m over the past 5 days. YTD flows are negative at -$17,717. The 5-day average is +$106m, the 20-day average of -$252m and the 100-day average of -$243m.

- India: Had outflows of -$518m as of the 9th, with total outflows of -$2,815m over the past 5 days. YTD flows are negative -$16,476m. The 5-day average is -$563m, the 20-day average of -$44m and the 100-day average of -$150m.

- Indonesia: Had outflows of -$13m as of Friday, with total inflows of -$313m over the prior five days. YTD flows are negative -$2,180m. The 5-day average is -$63m, the 20-day average -$43m and the 100-day average -$35m

- Thailand: Recorded outflows of -$34m as of Friday, outflows totaling -$250m over the past 5 days. YTD flows are negative at -$1,396m. The 5-day average is -$50m, the 20-day average of -$25m the 100-day average of -$18m.

- Malaysia: Recorded outflows of -$27m as of yesterday, totaling -$440m over the past 5 days. YTD flows are negative at -$2,778m. The 5-day average is -$88m, the 20-day average of -$60m the 100-day average of -$40m.

- Philippines: Saw inflows of +$1m as of Friday, with net outflows of -$78m over the past 5 days. YTD flows are negative at -$294m. The 5-day average is -$16m, the 20-day average of -$3m the 100-day average of -$6m.

OIL: US Energy Sec. Expects Lower Prices

- Iran and the US held indirect talks in Oman, discussing Iran's nuclear program and lifting of sanctions in a "constructive atmosphere" with "mutual respect".

- Oil opened Monday trading in Asia lower following the late surge on Friday stemmed the weekly losses.

- Oil’s surprise surge on Friday stemmed the downward movement of prices seen all week.

- WTI opened this morning at US$61.70 and weakened immediately to a low of $61.08 before steadying to $61.25

- Brent opened at $64.76 and reached a low of $64.35, before stabilizing at $64.54

- Oil markets are weighing the impact of the exemptions on tariffs on smartphones and other key electronic equipment.

- The US also indicated that ‘constructive’ conversations had occurred between the US and Iran over the weekend.

- Trump’s energy secretary Chris Wright says that under the Trump administration energy prices will be lower.

Gold Backs off From New Highs.

- Gold opened the week at US$3,237.61, a new high and rallied into the Asian trading morning to reach another new high of $3,245.75, before backing off to $3,230.70

- Goldman Sachs has raised it year end price target to $3,700, but warned in an extreme risk case, it could reach $4,500.

- Australia’s Northern Star Resources attempt to purchase the smaller De Grey Mining got a huge boost when Gold Road Resources (which owns 17% of De Grey) agreed to support the takeover (source BBG).

- Vietnam has discovered 12 new gold mines in the central region, containing more than 10 tonnes of gold and 16 tonnes of silver, following extensive geological surveys, the Mid-Central Geological Division said, VNExpress reported. (source BBG)

CHINA: Credit Growth Points to Positive Signs for the Economy.

- Over the weekend, China reported new loans data which pointed to positive signs for the domestic economy.

- China’s January-February New Yuan loans were CNY9.78tn versus an estimate of CNY9.14tn following prior period of CNY6.138tn.

- Aggregate financing was also strong up CNY15.18tn, from CNY9.292.1tn February.

- A stronger than expected lending to businesses coupled with very strong government bond issuance suggests that things are moving forward in an economy challenged by the weight of a downturn in property.

- The authorities have been clear in their intent of supporting the economy, as evidenced by the weight of government bond issuance.

- The PBOC’s deputy governor Xuan's speech while meeting with Japan and South Korean bank leaders last week, indicated China’s intent is to implement moderately loose monetary policy.

- What that is likely to look like could be a modest cut to the financing rate for 7-day reverse repurchase agreements via the open market operations and an expected cut the reserve requirement ratio (RRR) this quarter

CHINA: Exporters Get Ahead of Tariffs.

- China’s exports in USD terms outpaced estimates for March.

- Up in USD terms +12.4%, the result dramatically exceeded +4.6% estimates and the -3.0% February contraction.

- Of broader concern is the decline in imports, which contracted -4.3% YoY outpacing the forecast of -2.1%.

- The trade balance unsurprisingly surged to USD$102.6bn.

- The export data no doubt is inflated as exporters looked to get ahead of the tariffs now announced and March may prove to be an anomaly.

- The decline in imports speaks loudly as to the general malaise for the domestic consumer, something that is expected to predict further monetary policy easing soon.

CNH: USD/CNH Holding Above 7.3100, CNY Basket Remains In Sharp Downtrend

USD/CNH is holding above 7.3100 at this stage, close to session highs of 7.3173. We are around 0.30% weaker in CNH terms, while spot USD/CNY has pushed back above 7.3000 so far today. We continue to see meaningful divergence broader USD index trends. The BBDXY index is up from earlier lows though (from sub 1230, to be back near 1232).

- The USD/CNY fixing pushing up to multi year highs above 7.2100 suggests further gradual depreciation pressures in the yuan. The chart below shows the fixing and broader USD BBDXY breakdown.

- The authorities are likely to remain comfortable with further CNY basket weakness, as lower levels will help ease financial conditions. We had trade figures earlier, which showed higher than expected export growth, but significant uncertainties remain over the overlook given higher US tariff levels.

- CNH/JPY is up slightly from recent lows, last near 19.56, on Friday the pair dipped to 19.43. EUR/CNH was near 8.3200 in latest dealings, with recent highs near the 8.4000 level.

- China is likely to watch how Japan negotiations on trade unfold. Currency discussions may also feature, which has been hinted at by Japan officials.

- There still appears some distance between the US and China sides though. Market sentiment was buoyed by the late Friday news around tariff exemptions for key electronic products, but US President Trump said the whole electronics sector would still be subject to national security tariff related probe.

Fig 1: USD/CNY Fixing & USD BBDXY

Source: MNI - Market News/Bloomberg

INDONESIA: Country Wrap : FX Reserves Resilience Continues

- In positive development for Indonesia’s Sovereign Wealth Fund Danantara, Qatar has indicated it will invest jointly in the newly formed fund, up to US$2bn according to the State run news agency in Qatar (source BBG).

- Despite ongoing support for the rupiah in markets during periods of instability by the Central Bank, FX Reserves remained remarkably resilient in March.

- * After moderation in February, March FX reserves rose to US$157.1, setting a new record for reserves. It is the reserve accumulation that provides comfort that the BI can steward the economy through this period of volatility. The BI has intervened regularly of late as the rupiah fell to record lows. The IDR hit an all time low of 16,755, higher than the Asian crisis of 1997. Last week the deputy governor said that the BI will 'intervene boldly' in both onshore and offshore markets to stabilize the rupiah and maintain investor confidence. (source MNI – Market News).

- The Jakarta Composite is putting in another day of solid gains rising +2.00% following stronger than expected FX Reserve data.

- The rupiah did very little today, hovering at 16,787.

- Bonds had a less volatile day for a change with the 10YR slightly lower in yield at 7.06%

SOUTH KOREA: Country Wrap: KTBs into the WGBI

- South Korean smartphone and personal computer makers are staying cautious as unpredictable U.S. tariff policies increase uncertainty around their future production strategies. On Friday, U.S. administration exempted smartphones, computers and some other electronic devices from country-specific reciprocal tariffs, including the 125 percent levies imposed on Chinese imports. (source Yonhap)

- South Korean government bonds have secured final approval for inclusion in the FTSE World Government Bond Index (WGBI), one of the world’s top three sovereign debt benchmarks, although the entry date has been postponed to April 2026, index provider FTSE Russell said. The WGBI is one of the most widely used benchmarks in the world with approximately $3tn of funds managed relative to it. (source Chosun )

- The Kospi had a solid day rising +0.91% in a week where the Central Bank meets.

- The Won was one of the few regional currencies that fell today, down -0.5% to 1,427.62 on rate cut expectations from the BOK.

- Bonds were mixed across the curve with the 10YR at 2.71%

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 14/04/2025 | 1230/0830 | ** | Wholesale Trade | |

| 14/04/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 14/04/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 14/04/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 14/04/2025 | 1700/1300 | Fed Governor Christopher Waller | ||

| 14/04/2025 | 2200/1800 | Philly Fed's Pat Harker | ||

| 15/04/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 14/04/2025 | 2340/1940 | Atlanta Fed's Raphael Bostic | ||

| 15/04/2025 | 0130/1130 | RBA Meeting Minutes | ||

| 15/04/2025 | 0600/0700 | *** | Labour Market Survey | |

| 15/04/2025 | 0645/0845 | *** | HICP (f) | |

| 15/04/2025 | 0800/1000 | ** | ECB Bank Lending Survey | |

| 15/04/2025 | 0900/1100 | ** | Industrial Production | |

| 15/04/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 15/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 15/04/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 15/04/2025 | 1230/0830 | *** | CPI | |

| 15/04/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/04/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 15/04/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/04/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 15/04/2025 | 1300/0900 | * | CREA Existing Home Sales |