MNI EUROPEAN MARKETS ANALYSIS: Yuan Allowed To Weaken Again

- All eyes today on the USD/CNH as it broke above 7.40 in overnight trading. The market is looking for signs to confirm the PBOC is going to let the Yuan move lower. Chinese Premier Li Qiang said his country has ample policy tools to “fully offset” any negative external shocks.

- Cash US tsys have extended yesterday's decline during the Asia-Pac session. The sell-off reflects growing concerns that China may retaliate against tariffs by offloading US assets, including US tsys.

- The imminent and then actual introduction of US tariffs drove a sea of red across the region. The onshore equities bourses in China were the sole risers today as state owned asset managers bought the market with inflows into ETF’s linked to the ‘national team’ topped CNY87bn on Tuesday, an all time record.

MARKETS

US TSYS: Haven Demand Under Threat From China Retaliation

TYM5 is 110-12, +1-02 from closing levels in today's Asia-Pac session.

- Cash US tsys have extended yesterday's decline during the Asia-Pac session. The sell-off reflects growing concerns that China may retaliate against tariffs by offloading US assets, including US tsys.

- Alongside the steepening of the curve, interest-rate swaps have extended their recent extreme outperformance of US tsy securities as traders sought to avoid costs associated with holding bonds.

- Cash US tsys are currently trading 2-17bps cheaper across benchmarks, with the curve steeper.

- Yesterday, Trump officials confirmed the 104% tariff on China went into effect at noon. Concurrently, China vowed to "fight to the end".

- On the local front, the focus turns to the March FOMC minute release at 1400ET today, CPI on Thursday and PPI on Friday morning.

- Reminder, banks kick off the latest earnings cycle this Friday with Bank of New York Mellon, Wells Fargo & Co, JPMorgan Chase and Morgan Stanley reporting.

JGBS: Cheaper But Worst Levels, New Cycle High For Long End Bonds

JGB futures are stronger, +34 compared to the settlement levels, after reversing early afternoon session weakness.

- (MNI) The BoJ is closely analysing how US tariffs will affect Japan's economy and prices, amid growing uncertainty, Governor Kazuo Ueda told lawmakers on Wednesday.

- The BoJ will manage monetary policy in an appropriate manner, while carefully monitoring the economy, prices and financial markets, he added, without elaborating on how and when the bank might act.

- Today's weakness in JGBs has been primarily driven by moves in cash US tsys, which have extended their decline during today's Asia-Pac session. The sell-off reflects growing concerns that China may retaliate against tariffs by offloading US assets, including tsys.

- Yesterday, Trump officials confirmed the 104% tariff on China went into effect at noon. Concurrently, China vowed to "fight to the end".

- At present, cash US tsys are trading 3-12bps cheaper across the curve, with the curve steeper. Earlier, the US 30-year yield was up 26bps at 5.02%.

- Cash JGBs have twist-steepened, with yields 3bps lower to 11bps higher. The benchmark 30-year yield is 7.9bps higher at 2.595% after making a new cycle high of 2.809%, the highest since 2004, early in the afternoon session.

- The swaps curve has twist-steepened, with rates 10bps lower to 10bps higher. Swap spreads are tighter.

AUSSIE BONDS: Twist-Steepener Aligns With Global Bonds, RBA Gov Speech Tomorrow

ACGBs (YM +13.0 & XM -16.0) have twist-steepened, aligning with global markets.

- Cash US tsys are currently trading 1-15bps cheaper across benchmarks, with the curve steeper, extending yesterday's decline during the Asia-Pac session.

- The sell-off reflects growing concerns that China may retaliate against tariffs by offloading US assets, including US tsys.

- Alongside the steepening of the curve, interest-rate swaps have extended their recent extreme outperformance of US tsy securities as traders sought to avoid costs associated with holding bonds.

- Yesterday, Trump officials confirmed the 104% tariff on China went into effect at noon. Concurrently, China vowed to "fight to the end".

- On the US front, the focus turns to the March FOMC minute release at 1400ET today, CPI on Thursday and PPI on Friday morning.

- Cash ACGBs are 13bps richer to 18bps cheaper, with the 3/10 curve steeper and the AU-US 10-year yield differential at -2bps, 8bps tighter on the day.

- The bills strip has bull steepened with pricing +13 to +29.

- RBA-dated OIS pricing is 11-30bps softer across meetings today. A 50bp rate cut in May is given a 92% probability, with a cumulative 144bps of easing priced by year-end.

- Tomorrow’s local calendar will see Consumer Inflation Expectations data and a speech from RBA Governor Bullock.

BONDS: NZGBS: Twist-Steepener, RBNZ Cuts But US Long End Yields Rise

NZGBs closed with a dramatic twist-steepening of the curve, with yields 13bps lower to 21bps higher. The short-end finished at its yield lows, while the long-end finished at its yield high.

- The source of the move has been US tsys. Cash US tsys are currently trading 3-20bps cheaper across benchmarks, with the curve steeper.

- US long-end yields have risen for the third straight day amid growing cracks in the haven status of US government debt.

- Alongside the steepening of the curve, interest-rate swaps have extended their recent extreme outperformance of US treasury securities as traders sought to avoid costs associated with holding bonds.

- Yesterday, Trump officials confirmed 104% tariff on China went into effect at noon. Concurrently, China vowed to "fight to the end".

- Meanwhile, the RBNZ cut rates 25bp to 3.5% as was widely projected, due to significant spare capacity and a weaker outlook from “global trade policy” which should result in inflation staying close to the target mid-point.

- Swap rates closed 12bps lower to 14bps higher, with the 2s10s curve steeper and implied long-end swap spreads wider.

- RBNZ dated OIS pricing closed 1-10bps softer across meetings beyond April, with 117bps of easing by November 2025.

- Tomorrow, sell NZ$275mn of the 0.25% May-28 bond and NZ$225mn of the 4.25% May-34 bond.

RBNZ: “Scope” To Cut Further In Response To Tariff Impact

The RBNZ cut rates 25bp to 3.5% as was widely projected, due to significant spare capacity and a weaker outlook from “global trade policy” which should result in inflation staying close to the target mid-point. It also said that the economy had broadly developed as it expected in February when it forecast 50bp of easing in Q2. It sees “scope’ for further easing if “appropriate” and will be determined by “the outlook for inflationary pressure over the medium term”. At this stage further easing in May is likely, but size is less clear.

- “On balance” US tariffs are a downside risk to NZ growth and CPI inflation. Most of the MPC believed that trade policy announcements shifted risk around NZ’s inflation outlook to the downside, but some thought that they had increased uncertainty and as such risks “remain balanced at this stage”.

- It also noted that the recent weakening of the NZD would “help to cushion the immediate effect” for lower demand for NZ exports. It added that lower oil prices would not only reduce NZ inflation but also “support domestic consumption”. WTI is down another 3.5% today to be almost 20% lower in April.

- Tariffs will take time to be felt by the global economy and the possibility of further changes to what has only been recently announced adds to the uncertainty of their effect. The response of global supply chains is also unclear.

- The RBNZ observed that higher export prices and weaker kiwi had helped to support primary producers and add to NZ growth but private consumption and residential investment remain weak. However, the full effect of monetary easing to date is yet to be felt.

All eyes today on the USD/CNH as it broke above 7.40 in overnight trading. The market is looking for signs to confirm the PBOC is going to let the Yuan move lower. Chinese Premier Li Qiang said his country has ample policy tools to “fully offset” any negative external shocks.

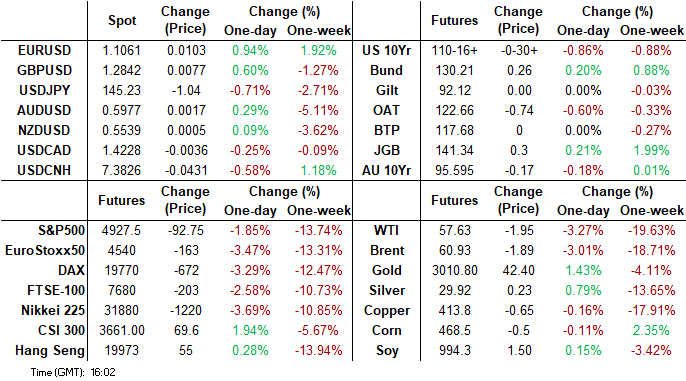

- EUR/USD - Asian range 1.0951 - 1.1066, going into the London open near the Asian highs around 1.1060. Quite a big range for the EUR in Asia as it benefits from the broad USD sell off.

- GBP/USD - 1.2762 - 1.2856, trading at the day's highs going into the London session. Look for sellers once more back towards 1.2900/50.

- USD/CNH - 7.3712 - 7.4273, finding some support back towards 7.3700 after falling away post the Yuan fix which printed 7.2066. The market views a higher USD/CNH as 1 of the cleanest ways to express 104% tariffs being applied. They need further confirmation from the PBOC to give the green light.

- USD/JPY - 144.58 - 146.36. USD/JPY has been under pressure most of the Asian session as Asian stocks tumbled. A bounce of its lows into the London session to be around 145.20, expect it to continue to trade heavy until we start seeing some actual trade deals done.

- Cross asset : SP -2.6%, Gold 3010.00 + 0.88%, US 10yr 4.42%, BBDXY 1264, Cruse oil 56.85

- Data/Events : FOMC minutes, ECB Knot speaks, ECB Cipollone speaks, BOE FPC meeting record released.

USDCNH

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Down Heavily Again After Yesterday’s Reprieve.

In a sea of red across the region, the onshore equities bourses in China were the sole risers today as state owned asset managers bought the market with inflows into ETF’s linked to the ‘national team’ topped CNY87bn on Tuesday, an all time record.

- The Hang Seng was down in line with other regional indexes, falling -1.55%, whilst the CSI 300 rose +0.30%, Shanghai +0.24% and Shenzhen +0.47% respectively.

- Taiwan’s TAIEX cratered today, falling -5.00% and is down over 15% in recent days.

- The KOSPI has fallen heavily again today after yesterday’ s modest gains, down -1.85%

- The FTSE Straits Times in Singapore was down -2.1%, and is approaching a decline of 15% over the last fortnight.

- Malaysia’s FTSE Bursa KLCI is down -2.7% today having finished virtually flat yesterday.

- The Jakarta Composite is down -0.33%, after yesterday’s decline of -7.90%

- India’s NIFTY 50 is down -0.60% in morning trading, after finishing strongly with gains of +1.6% yesterday.

ASIA STOCKS: Huge Outflows Across Major Markets.

With further tariff headlines spooking markets, data shows that the ongoing outflows from Asia equities continue.

- South Korea: Recorded outflows of -$483m as of yesterday, bringing the 5-day total to -$4,987m. 2025 to date flows are -$10,565, m. The 5-day average is -$997m, the 20-day average is -$260m and the 100-day average of -$154m.

- Taiwan: Had outflows of -$887m as of yesterday, with total outflows of -$411m over the past 5 days. YTD flows are negative at -$17,843. The 5-day average is -$82m, the 20-day average of -$397m and the 100-day average of -$243m.

- India: Had outflows of -$1,041m as of 7th, with total outflows of -$2,617m over the past 5 days. YTD flows are negative -$15,414m. The 5-day average is -$523m, the 20-day average of -$24m and the 100-day average of -$151m.

- Indonesia: Had outflows of -$228m as yesterday, with total inflows of -$32m over the prior five days. YTD flows are negative -$2,058m. The 5-day average is -$6m, the 20-day average -$36m and the 100-day average -$35m

- Thailand: Recorded outflows of -$71m yesterday, totaling -$230m over the past 5 days. YTD flows are negative at -$1,402m. The 5-day average is -$46m, the 20-day average of -$32m the 100-day average of -$19m.

- Malaysia: Recorded outflows of -$89m as of yesterday, totaling -$422m over the past 5 days. YTD flows are negative at -$2,664m. The 5-day average is -$84m, the 20-day average of -$67m the 100-day average of -$39m.

- Philippines: Saw outflows of -$7m as of yesterday, with net outflows of -$83m over the past 5 days. YTD flows are negative at -$292m. The 5-day average is -$17m, the 20-day average of -$3m the 100-day average of -$6m.

CROSS ASSET: Risk Parity - Breaking Pivotal Support Around 480

Over the last 15 years there has been a mass migration to passive funds in the trillions of USD’s. With the allure of low fees, broad diversification and liquidity, Risk Parity became the new buzz word.

- The Cons though are beginning to mount. Capital floods into the same names, amplifying market weightings.

- No fundamental discrimination, it will buy whatever the index holds regardless of Macro risks or price discovery. As long as money comes in the fund it continues to pay the highs.

- What happens in a bear market ? Redemptions spike and just like when they buy on the way up at the highs, there is no fundamental discrimination on execution so as redemptions hit the fund it will also sell at the lows.

- This can amplify downside risks to the market especially in the names that are most heavily held.

- Risk Parity was down another 1.73% overnight and is breaking a pivotal support area around 780 which could see an increase in redemptions and lock in a negative feedback loop. This bodes very poorly for stocks with a first target of around 680.

Risk parity index

Source: MNI - Market News/Bloomberg

OIL: Crude Sinks Further As US Tariffs Come Into Effect

Oil prices are down sharply again during today’s APAC session following confirmation that an additional 50% tariff on US imports from China would be charged and then the actual implementation of all reciprocal tariffs at midnight EST. China has not responded yet. There has been a general sell off across markets including commodities which are worried that increased protectionism will significantly reduce demand. The USD index is down 0.4%.

- WTI is down 4.4% to $57.00/bbl following yesterday’s 4.1% decline, remaining above initial support at $56.81. It is off its intraday low of $56.70. The benchmark is now down over 20.0% in April. Brent is 3.7% lower at $60.49 after approaching round-number support of $60 but only falling as far as $60.18. It is now over 19.0% lower this month.

- Price falls have been exacerbated by OPEC’s decision to increase output more than expected this month. At these levels many OPEC countries will face fiscal problems and US drillers won’t invest in new wells.

- Westpac’s Rennie said that if China doesn’t retaliate further, then Brent should be able to hold above $60/bbl (Bloomberg).

- Brent has shifted into bearish contago between December 2025 and December 2026 contracts, according to Bloomberg. Futures structures are showing market conditions easing significantly.

- Industry-based data showed a US crude inventory drawdown of 1.1mn barrels last week. Gasoline rose 200k while distillate fell 1.8mn. The official EIA data is out later today.

- Later the Fed’s Barkin speaks and March FOMC meeting minutes are published. The ECB’s Cipollone participates in a panel and BoE’s FPC meeting record is released.

Gold Rises Again as Equities Struggle

- Gold’s few uncertain days may be behind it as the rally began today as equities retreated.

- As tariff headlines abounded and having opened at US$2,984.58 gold rallied in the Asian trading afternoon back above $3,000 to be $3,009.00

- The White House has said that it will be pursuing tariffs of up to 104% on Chinese goods whilst Chinese Premier Li said that his country had ‘ample tools’ to “fully offset” the tariffs.

- Whilst gold enjoys ‘safe haven’ status amongst investors, in times of high volatility investors seek liquidity, something gold does not exhibit.

- Chinese investors put a record 7.6 billion yuan into gold-backed exchange-traded funds last week, seeking safety amid trade war tensions.

- Gold appears to be the only safe haven at present again as even treasuries are getting caught in the cross fire today.

INDIA: MPC Cut Rates by 25, Moves to Accommodative

- As expected the RBI cut rates by 25bps today in line with market consensus.

- This is the second cut from the RBI, following the cut at the prior meeting with all voting members in favour of the cut.

- At the press conference the governor noted that "On inflation front, while sharper than expected decline in food prices has given us comfort, we remain vigilant to possible risks from global uncertainty and weather disruptions. MPC noted that inflation below the target currently, supported by huge fall in food prices. Moreover, there is decisive improvement in inflation outlook. As per projections, there is now greater confidence of durable alignment of headline inflation with target of 4% over 12 months horizon," Sanjay Malhotra said

- The MPC has changed their policy stance from neutral to accommodative, reflecting the uncertainty in the global economy rather than the immediacy of inflation risks.

- He was clear to note that accommodative was to take off the table the idea of rate hikes.

MNI BSP Preview April 2025: BSP To Cut as Inflation Dips

- As inflation moderates further it now is at the bottom end of the BSP's range providing opportunity to reduce rates.

- Data has moderated with exports and imports lower and PMI's declining.

- The BSP had done a good job supporting the Peso and it is performing well relative to regional peers.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 09/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/04/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 09/04/2025 | - | Higher Reciprocal Tariffs On Imports | ||

| 09/04/2025 | 1230/1430 | ECB's Cipollone On Macro-Financial Stability Panel | ||

| 09/04/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/04/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 09/04/2025 | 1500/1100 | Richmond Fed's Tom Barkin | ||

| 09/04/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/04/2025 | 1800/1400 | *** | FOMC Minutes | |

| 10/04/2025 | 2301/0001 | * | RICS House Prices | |

| 10/04/2025 | 0130/0930 | *** | CPI | |

| 10/04/2025 | 0130/0930 | *** | Producer Price Index | |

| 10/04/2025 | 0600/0800 | *** | CPI Norway | |

| 10/04/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/04/2025 | 0800/1000 | * | Industrial Production | |

| 10/04/2025 | - | *** | Money Supply | |

| 10/04/2025 | - | *** | New Loans | |

| 10/04/2025 | - | *** | Social Financing | |

| 10/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 10/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 10/04/2025 | 1230/0830 | * | Building Permits | |

| 10/04/2025 | 1230/0830 | *** | CPI | |

| 10/04/2025 | 1300/1400 | BoE's Breeden at MNI Connect ‘UK economic and Financial Stability prospects’ | ||

| 10/04/2025 | 1330/0930 | Dallas Fed's Lorie Logan | ||

| 10/04/2025 | 1400/1000 | Kansas City Fed's Jeff Schmid | ||

| 10/04/2025 | 1430/1030 | ** | Natural Gas Stocks |