MNI US MARKETS ANALYSIS - Risk Rally Runs Out of Steam

Highlights:

- Risk rally runs of steam, with implications for growth, inflation from tariffs still looming large

- Earnings season to become a bigger factor from tomorrow, with big banks kicking off the quarterly cycle

- Fedspeak, US CPI up next - to be closely watched for tariff reaction function

US TSYS: 30s Sees Return Of Underperformance, Auction To Test Duration Demand

- Treasuries mostly trade firmer on the day, with gains led by 5s in a paring of yesterday’s risk-on moves seen after Trump further lifted tariffs on China but a broader 90-day pause and 10% reciprocal tariffs elsewhere.

- Cash yields are 6bp lower (5s) to 1bp higher (30s) on the day. 30s lag the decline after yesterday’s substantial flattening as the announcement helped further abate long-end deleveraging after a strong 10Y auction which saw a record high for indirect take-up. Today’s 30Y auction offers another litmus test of duration demand.

- In the interim, the US CPI report (preview) and jobless claims at 0830ET will be watched closely before a raft of Fedspeak plus of course continued sensitivity to US policy headlines

- Curves are mixed today, with 2s10s at 44bp (+0.5bp) broadly consolidating yesterday’s flattening from ~67bp pre tariff announcements but 5s30s at 77bp (+6.5bp) for a greater reversal back towards ~85bp pre-announcement.

- TYM5 trades at 111-02+ (+24) off an earlier high of 111-09 but still well within yesterday’s wide range. Cumulative volumes are elevated at 655k but low compared to recent overnight sessions.

- Yesterday’s low of 110-01 stopped short of trendline support at 109-30+ (drawn from Jan 13 low) whilst resistance is seen at 112-08 (Apr 8 high).

- Data: CPI Mar (0830ET), Real av hourly earnings Mar (0830ET), Weekly jobless claims (0830ET), Federal budget bal Mar (1400ET)

- Fedspeak: Logan (0930ET), Bowman nomination hearing (1000ET), Schmid (1000ET), Goolsbee (1200ET), Harker (1200ET) – see separate FED bullet

- Coupon issuance: $22B 30Y bond re-open - 912810UG1 (1300ET)

- Bill issuance: $85B 4W, $75B 8W bill auctions (1130ET)

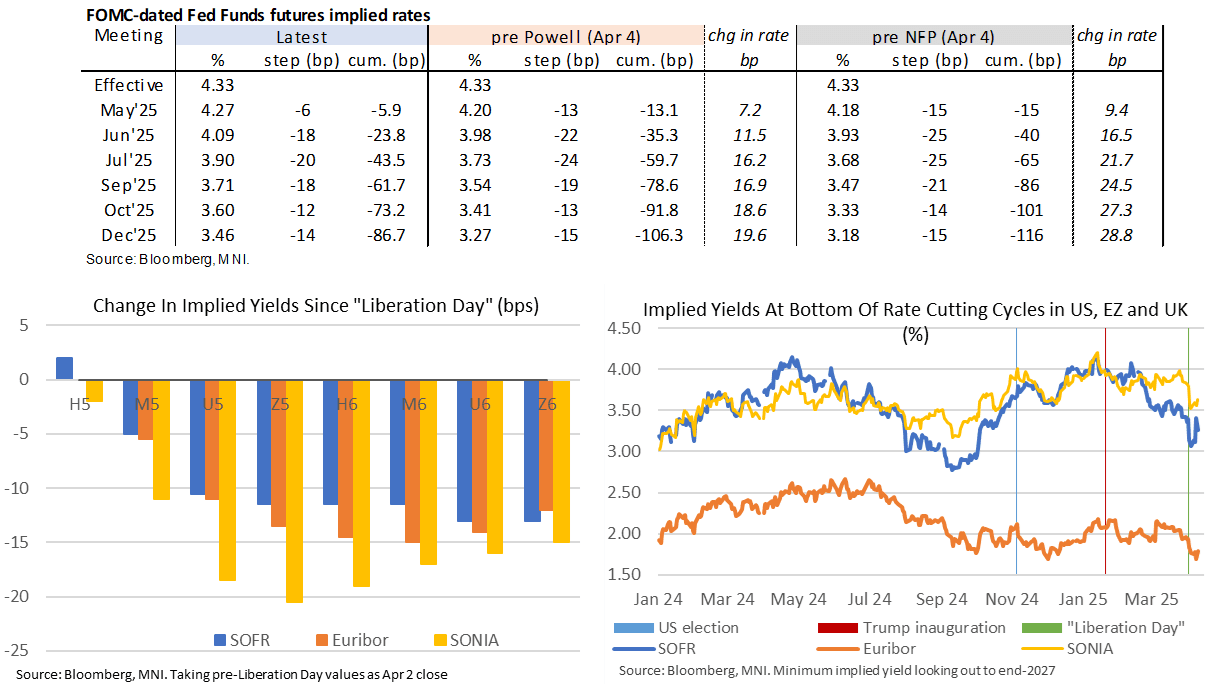

STIR: Fed Rates Pare Hawkish Shift, Still Very High Average Tariff Rate

- The Fed rate path has continued to pull back off yesterday’s hawkish extremes as part of the broader paring of risk touched in earlier comments.

- The 86bp of cuts priced for 2025 as a whole is down from yesterday’s 70bp although still a marked shift from ~100bp prior to Trump’s announcement.

- Cumulative cuts from 4.33% effective: 6bp May, 24bp Jun, 44bp Jul and 86bp Dec.

- Intermeeting cut odds are more negligible now, with FFJ5 showing just 1bp of cuts (vs as high as 6-7bp this week).

- In initial reaction yesterday, JPMorgan pushed their next Fed rate cut out to September from June previously but still see the top of the target range hitting 3.0% by 2Q26.

- Minneapolis Fed’s Kashkari (’26 voter) meanwhile sees a little less inflation impact if the tariff pause endures after yesterday’s dramatic changes although still sees a high bar for cutting rates.

- There’s much discussion about the still high average US tariff rate that’s in place and the caveat that it's now much more concentrated on China. For instance, JPM in yesterday’s reaction: “In static terms, today’s moves would actually increase the average effective tariff rate from 23% to 25%. But with Chinese tariffs going to punitive rates, even conservative estimates of the price elasticity of imports would suggest that China’s share of imports should shrink dramatically, taking down China’s contribution to the increase in the total average effective tariffs.”

- There’s a solid line-up of Fedspeak after today’s CPI report where we expect a continuation of patient rhetoric after various speakers yesterday. We expect the most hawkish commentary to come from Schmid (’25 voter) on the economy and policy at 1000ET (text tbd, Q&A) followed by Logan (’26 voter) at 0930ET albeit in welcoming remarks.

FED: Watching Schmid and Logan Amongst Today’s Solid Fedspeak Slate

- Minneapolis Fed’s Kashkari (’26 voter) offered the first FOMC official reaction to yesterday’s US escalation of China tariffs and broader 90-day pause. He sees a little less inflation impact if the tariff pause endures after yesterday’s dramatic changes although still sees a high bar for cutting rates, having earlier in the day published an essay arguing against moves in either direction (with the consideration of a hike helping build on the hawkish takeaway from his remarks).

- There’s a solid line-up of Fedspeak after today’s CPI report, where we expect a continuation of patient rhetoric after various speakers yesterday (Daly, Kashkari, Musalem and Barkin).

- We expect the most hawkish commentary to come from Schmid (’25 voter) on the economy and policy at 1000ET (text tbd, Q&A) followed by Logan (’26 voter) at 0930ET albeit in welcoming remarks. The two last spoke in February, an age ago considering the extent of recent developments:

- 0930ET – Logan (’26, hawk) welcome remarks at Dallas Fed event on “Outlook for North American Trade and Immigration”. She tends to focus on balance sheet matters although on Feb 14 said that even if inflation eases it doesn’t mean there’s room to cut rates.

- 1000ET – Bowman (permanent voter, hawk) Senate nomination hearing for VC Supervision role (text + Q&A). Whilst clearly going to be focused on financial regulatory matters, she noted on Mar 7 that the neutral rate has likely risen since the pandemic.

- 1000ET – Schmid (’25, hawk) on economic outlook and mon pol (text tbd, Q&A). He last spoke on Feb 27, with a huge amount changed since then, when he was focused on inflation and noted risks appeared to be to the upside.

- 1200ET – Goolsbee (’25, dove) at Economic Club of NY (text tbd, Q&A). The preeminent dove on the FOMC, he hinted at the importance of liaison programs on Apr 8, saying “we can’t really wait to the end of the quarter plus one month before we find out that investment really dropped off and GDP growth is shrinking, and we start seeing layoffs, unemployment, or on the other side, inflation starts soaring”. The day before he'd sounded his most hawkish in some time: "The anxiety is if these tariffs are as big as what are threatened on the US side, and if there’s massive retaliation, and then if there’s counter retaliation again, it might send us back to the kind of conditions that we saw in ‘21 and ‘22, when inflation’s raging out of control.”

- 1200ET – Harker (’26 role but retiring Jun’25, leaning dove) on fintech (text only). He said Mar 6 that with all this uncertainty, the Fed doesn’t want to move quickly. The economy was doing well but with some signs of concern.

- MNI US CPI Preview: https://media.marketnews.com/USCPI_Prev_Apr2025_de0699a656.pdf

MNI US EARNINGS SCHEDULE - Pre-Tariff Behaviour in Focus

- Financials take early focus this earnings season, with JPMorgan, Morgan Stanley, BNY Mellon, Wells Fargo and BlackRock all set to have reported by the end of this week.

- Goldman Sachs, Bank of America, Citigroup and others are set to follow next week.

- Markets will be particularly focused on any signs of front-loading corporate purchases ahead of expected tariffs, the rate at which firms will passthrough costs to the consumer and the expected impacts of tariffs on the bottom-line for consumer staples.

- Walmart have already this week withdrawn their quarterly income forecast given the uncertainty surrounding tariffs, however also stated that tariffs provide an opportunity to growth market share.

- This season will see over 50% of the S&P 500 having reported by the end of April, with the week beginning April 28th the busiest of the quarter.

US TSY FUTURES: Notable Reduction In Exposure On Wednesday

OI data points to meaningful net liquidation of Tsy longs during Wednesday’s sell off, with over $25mln of DV01 equivalent exposure shed across the curve.

- The most sizeable net positioning adjustment came in FV futures.

| 09-Apr-25 | 08-Apr-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 3,924,690 | 4,022,145 | -97,455 | -3,710,706 |

FV | 6,323,117 | 6,488,689 | -165,572 | -7,183,149 |

TY | 4,848,024 | 4,885,507 | -37,483 | -2,404,675 |

UXY | 2,306,954 | 2,354,791 | -47,837 | -4,251,702 |

US | 1,786,899 | 1,839,645 | -52,746 | -6,800,395 |

WN | 1,825,841 | 1,830,590 | -4,749 | -891,935 |

|

| Total | -405,842 | -25,242,563 |

STIR: Mix Of Short Setting & Long Cover Seen During Yesterday's SOFR Sell Off

OI data points to a mix of net short setting and long cover during yesterday’s sell off in SOFR futures, with the former dominating in the reds and greens and the latter more prominent in the whites and blues.

| 09-Apr-25 | 08-Apr-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,123,659 | 1,115,971 | +7,688 | Whites | -56,904 |

SFRM5 | 1,302,355 | 1,304,455 | -2,100 | Reds | +47,172 |

SFRU5 | 1,011,169 | 1,000,812 | +10,357 | Greens | +40,922 |

SFRZ5 | 1,085,754 | 1,158,603 | -72,849 | Blues | -9,049 |

SFRH6 | 677,923 | 684,719 | -6,796 |

|

|

SFRM6 | 771,541 | 736,853 | +34,688 |

|

|

SFRU6 | 695,975 | 684,871 | +11,104 |

|

|

SFRZ6 | 921,279 | 913,103 | +8,176 |

|

|

SFRH7 | 585,948 | 560,371 | +25,577 |

|

|

SFRM7 | 529,606 | 529,529 | +77 |

|

|

SFRU7 | 338,514 | 316,459 | +22,055 |

|

|

SFRZ7 | 429,605 | 436,392 | -6,787 |

|

|

SFRH8 | 268,383 | 262,751 | +5,632 |

|

|

SFRM8 | 190,477 | 201,252 | -10,775 |

|

|

SFRU8 | 141,648 | 144,717 | -3,069 |

|

|

SFRZ8 | 148,495 | 149,332 | -837 |

|

|

US-EU: VdL Confirms 90 Day Pause On Retaliatory Tariffs

European Commission President Ursula von der Leyen confirms earlier reports (see 'US-EU: Wires-EU Considers 90-Day Pause To 15 April Countermeasures: Diplos', 1108BST) of a 90 day pause on the EU's tariffs responding to US steel and aluminium levies, that were due to come into force on 15 April.

- VdL: "We took note of the announcement by President Trump. We want to give negotiations a chance. While finalising the adoption of the EU countermeasures that saw strong support from our Member States, we will put them on hold for 90 days. If negotiations are not satisfactory, our countermeasures will kick in. Preparatory work on further countermeasures continues. As I have said before, all options remain on the table."

- EU spox holding midday briefing presently. Livestream here. Trade spox Olof Gill says that, as he understands, EU will still face tariffs on autos, the 10% baseline, but not the 20% 'reciprocal' tariffs.

- Spox: 'I don't believe we require any additional legal [backing] from member states to go ahead with pause'. Reiterates that is his understanding, but he will need to check.

EUROPE ISSUANCE UPDATE:

UK: Consultation for next week's short-dated tender today

- The DMO has announced that it will hold the consultation for next Thursday's programmatic short-dated tender today with views sought by 13:00BST.

- It has announced that it will make a further announcement at 7:30BST tomorrow - with the gilt on offer likely to be announced then.

- This will be the first programmatic tender (i.e. one that is scheduled in the quarterly calendar). With other tenders the consultation is usually 3 days in advance with the announcement at 7:30 two days before - so this is earlier than usual. We would assume for now that all of the programmatic tenders will be announced on this schedule in future.

- We don't have a strong view regarding the gilt on offer. The 0.125% Jan-26 gilt (ISIN: GB00BL68HJ26) has been sold via tender three times since September for GBP1.5-2.0bln each time. That gilt matures in this fiscal year, so we are unsure if the DMO will still want to reopen it. That gilt is still trading at a decent premium indicating there is still scarcity, but the DMO may prefer to reopen a gilt with a slightly longer maturity.

Spain auction results

- Top of the range sold at that Spanish auction (E6.457bln vs E5.5-6.5bln target), with mixed results across lines.

- The 3.50% May-29 Bono results were relatively weak. The bid-to-cover ratio of 1.12x was lower than all 10 previous auctions for this line going back to October 2023. Meanwhile, the lowest accepted price of 103.960 was below the 103.963 pre-auction mid-price. The secondary market price for this Bono has nonetheless moved up to ~104.000 by around 09:50 BST, though.

- The on-the-run 3.15% Apr-35 Obli saw better results, with the bid-to-cover ratio of 1.90x exceeding last month’s 1.54x. However, only E1.970bln of this bond was sold today compared to E3.189bln in March. The low price of 98.280 comfortably exceeded the 98.158 pre-auction mid price.

- Today was the first re-opening of the 2.55% Oct-32 Obli since February 2023. The bid-to-cover of 1.83x was in line with that prior re-opening.

- E2.849bln of the 3.50% May-29 Bono. Avg yield 2.4622% (bid-to-cover 1.12x).

- E1.638bln of the 2.55% Oct-32 Obli. Avg yield 3.014% (bid-to-cover 1.83x).

- E1.97bln of the 3.15% Apr-35 Obli. Avg yield 3.349% (bid-to-cover 1.90x).

BOE: Amends Q2 '25 APF Schedule; Short Maturity Sale To Replace Long

The BOE has amended its Q2 '25 APF sales schedule: "In light of recent market volatility, the Bank will amend this schedule, and auction short maturity bonds on 14 April, instead of long maturity bonds. "

- "The Bank intends to reschedule the long maturity auction to the following quarter, in order to continue to reduce the APF as evenly as possible across maturity sectors, measured in initial proceeds terms. The schedule for Q2 is otherwise unchanged"

- This means that the BOE will hold two short dated operations in Q2 (in addition to the medium dated operation held on Monday). The original plan had been for one auction of each maturity bucket.

30-year Gilt yields fall ~2bp on that announcement to 5.41%. 2s30s flattens 1.5bps to 143.6bps.

FOREX: Risk Rally Lacks Follow-Through, USD Lower

- Unsurprisingly, European equities shot higher at the cash equity open Thursday, mimicking the record-setting Wednesday close on Wall Street. Markets have faded off highs, but are still maintaining a considerable rally on Trump's U-turn yesterday. US policy uncertainty remains well-elevated, with the US policy uncertainty index remaining at elevated levels, which continues to undermine the USD.

- The USD's initial rally has all but reversed, leaving EUR/USD at pre-U-turn levels. It is notable that the pair yesterday did not reverse as materially as equities did following the tariff pullback - which may be a strong signal that markets continue to discount the USD vs prior, pre-Liberation Day valuations, and that while tariff policy may have reversed, the implications for inflation and growth in the US this year persist.

- From a technical perspective, the trend condition in EURUSD is unchanged and remains bullish. Sights are on 1.1188 next, a Fibonacci projection. Initial firm support lies at 1.0854, the 20-day EMA.

- US CPI data is a focus going forward - although the risk premia surrounding the event have fallen notably since the tariff relief late yesterday. Markets expect 0.1% M/M, 2.5% Y/Y, but slightly higher prints in the core metrics.

- Several Fed speakers are set to make appearances Thursday: Fed's Logan, Schmid, Goolsbee and Harker are due, while the Senate are due to hold hearings on Bowman's nomination as the Fed's top banking supervisor.

OPTIONS: Expiries for Apr10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0900-10(E3.0bln), $1.0930-50(E3.0bln), $1.0960-65(E668mln)

- USD/JPY: Y143.00($1.3bln), Y145.00($744mln)

- EUR/GBP: Gbp0.8650-65(E643mln)

- AUD/USD: $0.6165(A$744mln), $0.6285($555mln), $0.6400(A$1.3bln)

- NZD/USD: $0.5600-05(N$724mln)

- USD/CAD: C$1.4395-00($1.5bln)

- USD/CNY: Cny7.3500($912mln), Cny7.4000($1.4bln)

COMMODITIES: Trend Condition for Gold Remains Bullish

- The trend condition in Gold remains bullish and the latest pull back appears to have been a correction. Moving average studies are unchanged, they remain in a bull-mode position highlighting a dominant uptrend.

- A bearish theme in WTI futures remains intact and yesterday’s rally from the day low is - for now - considered corrective. The move higher is allowing an oversold trend condition to unwind. Recent weakness has resulted in the breach of a number of important support levels.

EQUITIES: Volatility Clouds Technical Picture

- A short-term reversal in S&P E-Minis yesterday highlights the start of what appears to be a corrective cycle. The trend condition has been oversold following recent weakness and the move higher is allowing this set-up to unwind.

- Eurostoxx 50 futures have traded in an extremely volatile manner and rallied sharply higher from this week’s lows. The climb highlights the start of a corrective cycle and if this is correct, marks an unwinding of the recent oversold trend condition.

| Date | GMT/Local | Impact | Country | Event |

| 10/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 10/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 10/04/2025 | 1230/0830 | * | Building Permits | |

| 10/04/2025 | 1230/0830 | *** | CPI | |

| 10/04/2025 | 1300/1400 | BoE's Breeden at MNI Connect ‘UK economic and Financial Stability prospects’ | ||

| 10/04/2025 | 1330/0930 | Dallas Fed's Lorie Logan | ||

| 10/04/2025 | 1400/1000 | Kansas City Fed's Jeff Schmid | ||

| 10/04/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 10/04/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 10/04/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 10/04/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 10/04/2025 | 1600/1200 | Chicago Fed's Austan Goolsbee | ||

| 10/04/2025 | 1630/1230 | Philly Fed's Pat Harker | ||

| 10/04/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 10/04/2025 | 1800/1400 | ** | Treasury Budget | |

| 10/04/2025 | 2000/1600 | Boston Fed's Susan Collins | ||

| 11/04/2025 | 2301/0001 | ** | KPMG/REC Jobs Report | |

| 11/04/2025 | 0600/0700 | ** | UK Monthly GDP | |

| 11/04/2025 | 0600/0800 | *** | Final Inflation Report | |

| 11/04/2025 | 0600/0700 | ** | Trade Balance | |

| 11/04/2025 | 0600/0700 | ** | Index of Services | |

| 11/04/2025 | 0600/0700 | *** | Index of Production | |

| 11/04/2025 | 0600/0800 | *** | HICP (f) | |

| 11/04/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 11/04/2025 | 0700/0900 | *** | HICP (f) | |

| 11/04/2025 | 0945/1145 | ECB's Lagarde at Eurogroup Press Conference | ||

| 11/04/2025 | - | *** | Money Supply | |

| 11/04/2025 | - | *** | New Loans | |

| 11/04/2025 | - | *** | Social Financing | |

| 11/04/2025 | - | BoE's Saporta on 'How financial crisis reshape market and strategies’ | ||

| 11/04/2025 | 1230/0830 | *** | PPI | |

| 11/04/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 11/04/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 11/04/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 11/04/2025 | 1500/1100 | New York Fed's John Williams | ||

| 11/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |