MNI US OPEN - US, China Trade Talks to Start This Week

EXECUTIVE SUMMARY

- MNI FED PREVIEW - WHEN IN DOUBT, WAIT IT OUT

- US-CHINA TRADE TALKS TO START THIS WEEK FOCUSED ON DE-ESCALATION

- INDIA, PAKISTAN TRADE MILITARY STRIKES AFTER KASHMIR ATTACK

- CHINA TO SUPPORT STOCK MARKETS FURTHER

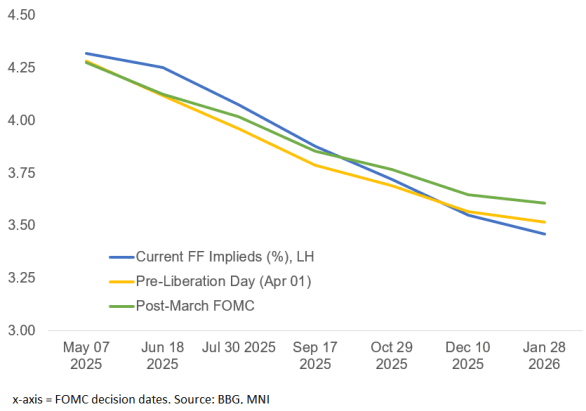

Figure 1: FOMC Meeting-Dated Fed Funds-Implied Rate Paths (%)

CENTRAL BANK PREVIEWS

MNI FED PREVIEW - MAY 2025: When in Doubt, Wait It Out

The FOMC will extend its series of rate holds to a third meeting in May, keeping the Fed funds target rate at 4.25-4.50% while maintaining its forward guidance in the Statement. It has been an eventful six weeks since the prior decision which included escalation and subsequent partial backtracking in US tariff policy, and the impact of uncertainty on economic sentiment (if not yet the “hard” data). As the FOMC awaits clarity in both government policy and the data on the degree to which one if not both dual mandate targets will be missed, most participants will continue to support a holding pattern until there is a clearer signal to act. See a summary of analyst views here.

MNI BOE PREVIEW - MAY 2025: Could “Gradual” Be Dropped?

Going into this week’s meeting an outcome other than a 25bp cut would be surprising but there will be a number of things to watch: any changes to the guidance and the inflation / growth forecast changes, the vote split and the introduction of new scenarios. For the guidance we expect "restrictive" and "careful" to remain but we question whether "gradual" will be removed and talk through the rationale for this potential change.

MNI RIKSBANK PREVIEW - MAY 2025: Scope for Dovish Tilt

The Riksbank is expected to keep rates on hold at 2.25% on May 8. Although the May decision does not include an updated set of macroeconomic forecasts and rate path projection, we still think there is scope to open the door to another rate cut later this year, conditional on downside growth risks materialising.

MNI NORGES BANK PREVIEW - MAY 2025: Still Holding Steady

Norges Bank is widely expected to keep policy rates on hold at 4.50% on May 8. Rates have been at this level since December 2023, after the Board opted to go against prior guidance for a cut in March due to an acceleration in inflationary pressures at the start of this year. Analysts are unanimous in projecting rates to be held at 4.50% in May, with limited expectations for any guidance changes in the policy statement. Most analysts expect 2x25bp cuts in 2025, with September the most likely start date.

MNI NBP PREVIEW - MAY 2025: Locked & Loaded

The National Bank of Poland will reduce interest rates this week for the first time since October 2023. The recent streak of expectation-missing inflation, labour market and economic activity data have created a conducive environment for looser monetary policy. An abating risk of a rebound in energy prices in 4Q25 further supports the case for the long-awaited launch of an easing cycle. We align with consensus and market pricing in seeing a 50bp rate cut as the most likely outcome of this week’s MPC meeting but see two-sided risks to this baseline scenario.

MNI CNB PREVIEW - MAY 2025: Close Call

The Czech National Bank may be nearing the end of its rate-cutting cycle, but fine-tuning the repo rate by another 25bp to 3.50% is on the table, even though it would likely be framed as a “hawkish cut”. Below-target inflation reported on the eve of the meeting supports the case for an imminent cut, but the underlying structure of inflationary pressures may strengthen the Bank Board’s determination to turn more cautious going forward.

MNI BCB PREVIEW - MAY 2025: Tightening Cycle Nearing End

The Copom is expected to deliver a smaller 50bp Selic rate hike on Wednesday to 14.75%, consistent with the guidance for a slowdown in the tightening pace from prior 100bp increments. Governor Galipolo recently said the board is responding to an inflation dynamic that is challenging, and that the current tightening bias in place remains valid. However, given an uncertain external outlook that demands caution and a well-behaved BRL, a below-consensus 25bp hike should not be ruled out.

MNI BNM PREVIEW - MAY 2025: On Hold for Now

The implications of tariffs from the US remains unclear. Inflation has softened further, yet upside risks are present given the trade war. Domestic consumption remains robust and the recent delay in the GST hike is supportive of the consumer.

NEWS

US/CHINA (BBG): US-China Trade Talks to Start This Week Focused on De-Escalation

US Treasury Secretary Scott Bessent and US Trade Representative Jamieson Greer will travel later this week to Switzerland for trade talks with China led by Vice Premier He Lifeng, seeking to de-escalate a tariff standoff that has threatened to hammer both economies. The travel was announced in statements Tuesday from the Chinese and US governments. It will be the first confirmed trade talks between the countries since President Donald Trump announced punishing levies of as high as 145% on China that were met with retaliatory rates of 125% from Beijing.

INDIA/PAKISTAN (BBG): India, Pakistan Trade Military Strikes After Kashmir Attack

India conducted targeted military strikes against Pakistan, which said it retaliated in expected tit-for-tat blows after a militant attack last month in Kashmir that killed 26 people. India said in a statement early Wednesday that it conducted “a precise and restrained response” that was “designed to be non-escalatory in nature.” The strikes hit nine targets in its neighbor, officials in India said at a briefing later in the day, and were the deepest breach of Pakistani territory since the 1971 war.

CHINA (MNI): China to Support Stock Markets Further

Chinese authorities will enhance stock market support via increasing liquidity and easing regulations, officials told reporters on Wednesday in a briefing. In addition, The PBoC will cut banks’ reserve requirement ratio by 50 bps and its seven-day reverse repurchase operation rate by 10 basis points. On housing, China will cut the loan rates of the individual housing provident fund by 0.25 percentage points, in a bid to support home purchase demand and stabilise the property market.

CHINA/RUSSIA (MNI): China and Russia Put Stalled Gas Pipeline on Moscow Talks Agenda

Talks between Chinese leader Xi Jinping and Russia’s Vladimir Putin this week will include negotiations around a much-delayed natural gas pipeline connecting the two economies, reviving discussions hampered for years by disagreements on the cost, route and urgency of the project. Moscow has long sought to secure a deal on the Power of Siberia 2 link — to tighten ties, but also to increase gas flows to the world’s largest energy importer.

GERMANY (MNI): Pistorius Seeks E60bln/Year for Defence as Merz Visits Paris & Warsaw

Reuters reports that Defence Minister Boris Pistorius is seeking a significant increase in Germany's annual defence budget, according to two of its sources. Pistorius, who hails from the centre-left Social Democrats (SPD) and in opinion polling is one of Germany's most popular politicians, is aiming for more than E60bln per year in new defence spending from 2025 onwards, according to one of the sources. SIPRI reports German defence spending came in at USD88.5B in 2024.

EU (MNI EXCLUSIVE): EU Escape Clauses Linked to Trade, NATO Talks - Officials

US/UK (FT): UK Closes in on US Trade Pact With Lower Tariff Quotas for Cars and Steel

The UK and the US are close to agreeing a trade pact that would cushion the impact of Donald Trump’s “liberation day” tariffs by granting lower-tariff quotas for British car and steel exports, according to officials in London and Washington. The deal — set to be signed this week — is due to include quotas that spare some UK exports from the full brunt of the additional 25 per cent tariffs that Trump levied on steel and car imports in February and March.

UK (The Times): Investors in UK Dump Bonds at Fastest Rate in Five Years

Investors in Britain dumped bonds at the second highest rate on record as tariff wars raised expectations of an emergency US interest rate cut and cash was raised to meet margin calls caused by market turmoil. Just over £1.2 billion was pulled from fixed income funds in April, according to data from Calastone, the global funds network, the fastest pace since the early days of the pandemic in April 2020.

PHILIPPINES (BBG): Philippines Signals It Won’t Intervene to Cap Peso Strength

Philippine central bank Governor Eli Remolona signaled authorities are unlikely to intervene to curb the strength in the peso, sending the local currency to the highest in more than a year. “This is a story of dollar weakness,” Remolona said in a mobile-phone message on Wednesday. “To intervene now would be to go against the tide.”

SOUTH KOREA (MNI): Won’t Stand for Presidency if PPP Doesn’t Agree to Unity Ticket - Han

Former PM and acting President Han Duck-soo has said that if he and the candidate for the conservative People Power Party (PPP) cannot agree to team up ahead of the 3 June presidential election, then he will not run for the presidency. Han has talked up the idea of running on a joint ticket with former labour minister Kim Moon-soo/ In recent days Han has attempted to distance himself from the presidency of the now-impeached Yoon Suk-yeol, arguing that "I was always against martial law," but criticising the 30+ impeachments against gov't ministers and officials brought by the opposition liberal Democratic Party of Korea (DPK).

DATA

EUROZONE DATA (MNI): March Retail Sales Broadly Flat, Non-Food Continues to Carry Y/Y

- EUROZONE MAR RETAIL SALES -0.1% M/M, +1.5% Y/Y

Eurozone (real) retail sales were overall broadly unchanged in March, at -0.1% M/M (+0.1% M/M cons; +0.2% February, revised from +0.3%). Across sectors, auto fuel was the only positive M/M print, at +0.4% M/M; both "non-food products except automotive fuel" and the food/drinks/tobacco category printed -0.1% M/M. On a longer-term Y/Y comparison, non-food sales (excl. fuel) continue to be the largest upside contributor. The total Y/Y was softer than in February at +1.5% in March vs +1.9% prior, revised from +2.3%.

GERMANY DATA (MNI): Factory Orders Strong in March

German factory orders were comparably strong in March, at 3.6% M/M (vs 1.3% cons, 0.0% prior). Overall, the data appears to indicate that the industrial sector in Germany was off cycle lows towards the end of Q1 - sentiment has also increased recently and the higher infrastructure / military government spending will provide some relief in due time, the broad-based decline until mid-24 seems to have halted for a while now. Despite this, we remain cautious if this represents a major turning point and the release does not suggest factory orders will soon print at cycle highs again.

GERMANY DATA (MNI): VDMA Machinery Data Underpins Strong March Factory Orders Print

VDMA machinery orders printed +4% Y/Y in March, bringing in Q1 orders in the sector at +4% Y/Y, also. This was the first quarter since Q1'22 with an incline on the yearly rate. VDMA sees an inflection point for foreign orders but does flag uncertainty about the further trajectory there - "particularly with regard to the USA's tariff policy and possible countermeasures". "The weakening domestic business (minus 3 per cent) was offset by a 6 per cent increase in foreign orders", VDMA comments.

FRANCE DATA (MNI): Employment Prospects Soft; Q1 Wage Pressures Ease

French employment prospects remain soft. Private sector payrolled employment was flat in Q1, according to preliminary estimates, while annual growth was -0.3% Y/Y (vs -0.1% prior). This softening in employment is consistent with recent falls in the EC's Expected Employment Indicator, which has broadly been seen across industries.

SWEDEN DATA (MNI): Lower-Than-Expected April Flash Inflation; RB Guidance Tilt Possible

- SWEDEN FLASH APR CPIF +2.3% Y/Y

Swedish April flash inflation was lower than analyst forecasts: Headline CPIF at 2.3% Y/Y vs 2.29% Riksbank, 2.4% consensus and CPIF ex-energy at 3.1% Y/Y vs 3.15% Riksbank, 3.2% consensus. Consensus for CPIF ex-energy was skewed towards a firmer 3.2/3.3% reading, so the downward surprise is notable. However, there are no details provided in the flash release. As such, this shouldn't have a major impact on today's Riksbank Executive Board meeting and tomorrow's policy rate decision. On the margin, it may increase the likelihood of a dovish guidance tilt, opening the door to a cut later this year conditional on downside growth risks materialising (which is our expectation).

NEW ZEALAND DATA (MNI): NZ Unemployment Holds at 5.1% in Q1

New Zealand’s unemployment rate held steady at 5.1% over Q1, 10 basis points lower than expected, Stats NZ data showed Wednesday. The underutilisation rate was 12.3%, compared with 12.1%, while the employment rate was 67.2%, down from Q4’s 67.3%. The Reserve Bank of New Zealand had expected unemployment to reach 5.2% in Q1 before tightening to 4.9% by the December quarter.

FOREX: Greenback Stable Above Lows on US-China Trade Talks

- The greenback is more stable above yesterday's low, seeing support from yesterday's late reports that US-China trade talks will commence by the end of the week. This has tipped USD/JPY well off yesterday's lows and back above the Y143.00 handle. Nonetheless, the primary trend direction in USDJPY remains bearish and gains since Apr 22 appear corrective. Resistance at the 50-day EMA, at 146.33, remains intact.

- Meanwhile, GBP/USD has faded further off the Tuesday high, putting prices through the overnight low as well as 1.3329 - the 38.2% retracement of the downleg posted off the Apr28 high. The BoE decision due tomorrow should prove influential here, with the MPC seen opting for another 25bps rate cut.

- The Fed decision due later today is expected to be one of the least consequential of the year, with no change in policy expected as the FOMC look through recent market volatility and await hard economic data in the coming few months to make a decision on rates. Markets price scant chance of any move today, with the next 25bps step lower seen at the July meeting, once we get the first insight into economic behaviour post-tariffs via the NFP and CPI reports.

- Trump's schedule Wednesday is relatively light, however much focus may be paid to his participation in the swearing in ceremony for David Purdue as the US ambassador to China - often seen as a critic of China.

EGBS: Futures Rally to Fresh Session Highs; Brush Aside German Spending Sources

Major EGB futures have rallied to fresh session highs over the last 60 minutes, led by semi-core/peripherals. The space largely brushed aside a Reuters sources article detailing German defence spending plans, with the piece lacking clarity on whether the touted E60bln of additional spending is for 2025 alone or split across the current parliamentary term.

- The limited reaction in German swap spreads suggests the story is consistent with pre-existing sell-side estimates of defence spending increases.

- Bund futures are +16 ticks at 131.07, with initial resistance seen at 131.24 (Apr 5 high). That shields key resistance and the bull trigger at 132.03 (Apr 7 high).

- OAT and BTP futures are up ~25 ticks each, with no obvious driver of outperformance versus Bunds. Today’s LT OAT auction was solid, but doesn’t seem to be enough to account for the outperformance.

- The German curve has bull flattened, with 30-year yields 3bps lower on the session. 10-year EGB spreads to Bunds are now up to 2bps tighter.

- Italy has held a buyback transaction this morning.

- Eurozone March retail sales were in line with consensus at -0.1% M/M, vs a one tenth downwardly revised 0.2% prior.

- Global macro focus turns to this evening's FOMC decision.

GILTS: Rallying Alongside Peers

Gilts have rallied alongside core global FI markets in recent trade, we continue to search for an overt driver.

- Although demand at the latest OAT & gilt auctions was deemed solid to strong, the results don’t seem firm enough to account for the rally.

- Meanwhile, oil futures have moved away from session highs, but the pullback has is only modest at this stage.

- Futures have registered fresh session highs of 93.15 in recent trade.

- Next resistance of note located at the May 2 high (93.93).

- Yields 0.5-4.0bp lower, flattening bias on the curve

- 10s 1bp tighter vs. Bunds, after holding between 195-200bp in closing terms over the last 3 sessions.

- Last week’s yield lows intact across the curve, 10s last 4.49%, ~8bp off their ’25 base.

- GBP STIRs hold close to opening levels, with ~95bp of cuts priced through year-end and the next 25bp cut fully discounted come the end of tomorrow’s decision.

- Expect macro and cross-market cues to dominate for much of today’s session, although signs of thawing Sino-U.S. tensions, reports of advances in UK-U.S. trade talks and Chinese macro policy easing have had little lasting impact thus far.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

May-25 | 4.201 | -25.9 |

Jun-25 | 4.070 | -38.9 |

Aug-25 | 3.871 | -58.9 |

Sep-25 | 3.731 | -72.9 |

Nov-25 | 3.572 | -88.7 |

Dec-25 | 3.513 | -94.6 |

EQUITIES: Bullish Conditions in E-Mini S&P Remain Intact

Eurostoxx 50 futures maintain a positive tone and the contract is trading at its recent highs. Price has recently cleared both the 20- and 50-day EMAs, and attention is on 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. This hurdle has been pierced, a clear break of it would pave the way for a climb towards 5341.00, the Mar 27 high. Initial support to watch lies at 5082.47, the 20-day EMA. Clearance of this level would signal a possible reversal. Bullish conditions in S&P E-Minis remain intact. The contract has breached the 50-day EMA, at 5622.98. A continuation of the bull phase would expose 5837.25 next, the Mar 25 high and a bull trigger. It is still possible that the entire rally since Apr 7 is a correction. A reversal lower would signal the end of this corrective phase and expose initially, support at 5127.25, the Apr 21 low. First support to watch is 5536.59, the 20-day EMA.

- Japan's NIKKEI closed lower by 51.03 pts or -0.14% at 36779.66 and the TOPIX ended 8.38 pts higher or +0.31% at 2696.16.

- Elsewhere, in China the SHANGHAI closed higher by 26.551 pts or +0.8% at 3342.665 and the HANG SENG ended 29.17 pts higher or +0.13% at 22691.88.

- Across Europe, Germany's DAX trades higher by 6.89 pts or +0.03% at 23260.65, FTSE 100 lower by 32.57 pts or -0.38% at 8565.26, CAC 40 down 38.11 pts or -0.5% at 7659.26 and Euro Stoxx 50 down 9.66 pts or -0.18% at 5254.19.

- Dow Jones mini up 212 pts or +0.52% at 41128, S&P 500 mini up 33 pts or +0.59% at 5656.75, NASDAQ mini up 125.75 pts or +0.63% at 19996.25.

Time: 10:00 BST

COMMODITIES: Recent Recovery for Gold Could Signal End of Correction Lower

A medium-term bearish trend in WTI futures remains intact and short-term gains are considered corrective. The move down that started Apr 23 signals the end of the correction between Apr 9 - 23. That cycle higher allowed an oversold condition to unwind. Attention is on $54.67, the Apr 9 low and a bear trigger. Clearance of this level would resume the downtrend and open $53.72, a Fibonacci projection. Key resistance to watch is $64.12, the 50-day EMA. Gold has recovered from its recent lows and this suggests the correction between Apr 22 - May 1, is over. A continuation higher would refocus attention on key resistance and the bull trigger at $3500.1, the Apr 22 high. Clearance of this level would confirm a resumption of the primary uptrend. Key short-term support has been defined at $3202.0, the May 1 low. A break of this level is required to signal scope for a deeper retracement.

- WTI Crude up $0.9 or +1.52% at $60

- Natural Gas up $0.11 or +3.06% at $3.569

- Gold spot down $48.86 or -1.42% at $3382.72

- Copper down $4.85 or -1.02% at $473

- Silver down $0.33 or -1.01% at $32.8891

- Platinum down $0.44 or -0.04% at $987.26

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 07/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 07/05/2025 | 1400/1000 | Treasury Secretary Scott Bessent | ||

| 07/05/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 07/05/2025 | 1800/1400 | *** | FOMC Statement | |

| 07/05/2025 | 1900/1500 | * | Consumer Credit | |

| 08/05/2025 | - | NorgesBank Meeting | ||

| 08/05/2025 | 0600/0800 | ** | Trade Balance | |

| 08/05/2025 | 0600/0800 | ** | Industrial Production | |

| 08/05/2025 | 0700/0900 | ** | Industrial Production | |

| 08/05/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 08/05/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1130/1230 | BOE Press Conference | ||

| 08/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 08/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 08/05/2025 | 1230/0830 | ** | Preliminary Non-Farm Productivity | |

| 08/05/2025 | 1300/1400 | Decision Maker Panel data | ||

| 08/05/2025 | 1400/1000 | BOC Financial Stability Report and Financial System Survey | ||

| 08/05/2025 | 1400/1000 | ** | Wholesale Trade | |

| 08/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 08/05/2025 | 1500/1100 | BOC Governor Macklem press conference on Financial System Review | ||

| 08/05/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 08/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 08/05/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 08/05/2025 | 1700/1300 | * | US Treasury Auction Result for Cash Management Bill |