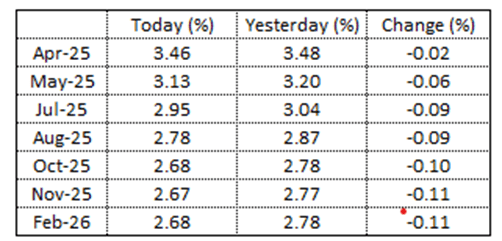

STIR: RBNZ Dated OIS Pricing Softer Ahead Of RBNZ Policy Decision

RBNZ dated OIS pricing is 2-11bps softer across meetings.

- 29bps of easing is priced for today, with a cumulative 109bps by November 2025

Figure 1: RBNZ Dated OIS Today vs. Yesterday (%)

Source: MNI – Market News / Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Subdued Session On A Data-Light Day

ACGBs (YM -1.0 & XM -1.5) are modestly cheaper on a data-light session.

- Cash US tsys are 2-3bps richer across benchmarks in today’s Asia-Pac session as Asian traders digest Friday’s US jobs data and remarks from Federal Reserve Chair Jerome Powell.

- Cash ACGBs are 1bps cheaper with the AU-US 10-year yield differential at +14bps.

- Swap rates are flat to 1bp higher.

- The bills strip is flat to -2 across contracts.

- RBA-dated OIS pricing is little changed across meetings today.

- Nevertheless, pricing remains mixed compared to February’s pre-RBA Decision levels—meetings through May are 3-4bps firmer, while those beyond are 1-14bps softer. A 25bp rate cut in April is given a 9% probability, with a cumulative 64bps of easing priced by year-end (based on an effective cash rate of 4.09%).

- This week, the AOFM plans to sell A$300mn of the 2.75% 21 May 2041 bond tomorrow and A$800mn of the 3.50% 21 December 2034 bond on Wednesday.

CROSS ASSET: US Related Assets Struggle, As Trump Doesn't Rule Out Recession

US exceptionalism trades continue to be unwound in the first part of Monday trade. However, we are away from recent extremes for key benchmarks (US equity futures, Tsy yields and the USD index). Weekend comments from US President Trump, which didn't rule out a US recession this year, have weighed on US related assets.

- BBG notes: "Asked on Fox News’ Sunday Morning Futures whether he’s expecting a recession this year, Trump said, “I hate to predict things like that. There is a period of transition, because what we’re doing is very big.” (see this link for more details).

- Measures of US recession probability risks have ticked higher, with Polymarket odds firming back towards recent highs. The US policy uncertainty index sits off recent elevated levels.

- US equity futures opened sharply weaker, Eminis down over 1%,although losses are now back at -0.50%. We are still above recent lows. In contrast, EU futures have opened higher, up over 0.80% at this stage.

- US tsys yields have ticked lower, the 10yr off close to 3bps, last near 4.27%, while the 2yr was back under 4%.

- The USD has softened, with the yen outperforming. The BBDXY index is off a further 0.10% to 1266.6. We are just up from recent lows for this index (1264.80). USD/JPY has slumped to 147.30, eyeing a re-test of 147.00.

- Earlier comments from Trump stated he thinks a government funding lapse probably won't happen. He also expressed optimism around Ukraine talks and TikTok's sale.

CHINA PRESS: CPI Could Recover In March

China’s consumer price index is expected to reach 0.3% y/y in March, up from February’s 0.7% fall, according to Feng Lin, director of research at Orient Jincheng, citing recent trends in high-frequency data and the current consumer market supply and demand balance. Looking ahead, Mingming, chief economist at CITIC Securities, said PPI y/y declines may narrow from February's 2.2% fall, as demand increases and ferrous industry prices gain momentum, however geopolitics brings uncertainty. (Source: Securities Daily)