CNH: USD/CNH Eyeing 20-day EMA Resistance Post Fresh Tariff Comments

USD/CNH spiked from the low 7.2700 region to above 7.2900 late in US Thursday trade as renewed tariff threats from US President Trump crossed. We sit around 7.2940 in early Friday dealings. We are close to the 20-day EMA resistance, which is near 7.2960. A move back above this level would likely see 7.3000 targeted, while pre Trump inauguration levels were back above 7.3300. On the downside, we are back above the 50-day EMA resistance (near 7.2835), but the 100-day EMA, which is further south, close to 7.2510, is likely a more important support zone.

- Trump wasn't specific in terms of tariff threats on China, in wide ranging remarks delivered late on Thursday US time. He stated “With China, I’m also thinking about something because they’re sending fentanyl into our country, and because of that, they’re causing us hundreds of thousands of deaths,” Trump said Thursday. “So China is going to end up paying a tariff also for that, and we’re in the process of doing that.” (per BBG, see this link).

- The remarks followed earlier comments that tariffs would be imposed on Mexico and Canada, with drug flows, immigration and trade deficits cited as factors.

- China onshore markets are closed until next Wednesday for the LNY break, which will leave CNH without an onshore anchor point. Hong Kong markets also remain closed today.

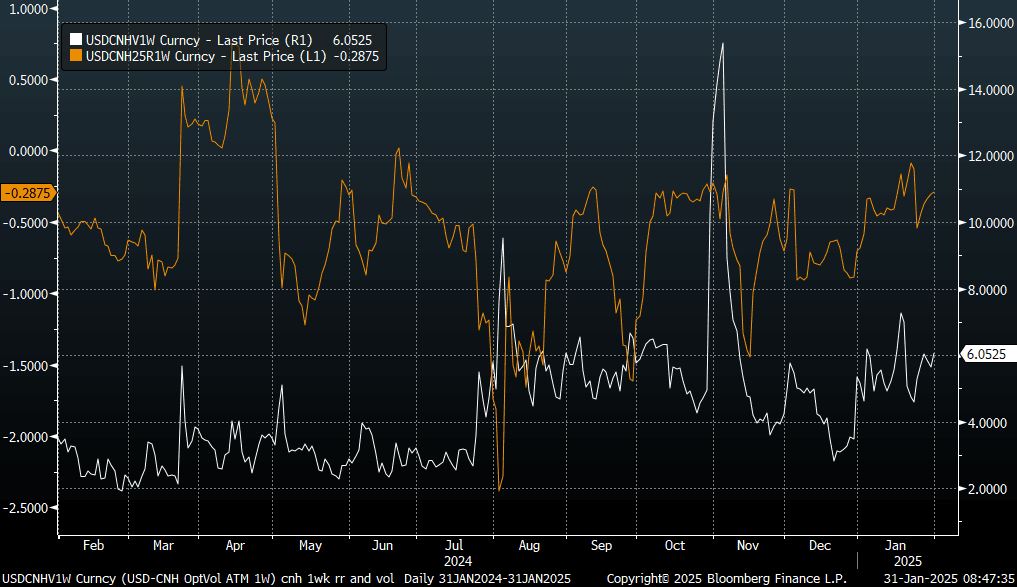

- 1 week implied vols and risk reversals are higher, but still sub pre inauguration levels, see the chart below.

Fig 1: USD/CNH 1week Implied Vol and Risk Reversal Trends

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Tsy Curves Look To Finish 2024 at June'22 Highs

- Treasuries look to finish the last trading session of 2024 lower after reversing Tuesday morning support. Markets closed Wednesday for New Years day, resume full trade Thursday.

- The Mar'25 10Y contract trades 108-25.5 (-5.5) late in the day, 10Y yield near session high of 4.5871%. Curves bounced off flatter levels, 2s10s climbing to 34.344 -- the highest level since June 2022.

- Short end support, in turn, helped projected rate cuts into early 2025 gain momentum vs. late Monday levels (*) as follows: Jan'25 steady at -2.8bp, Mar'25 -14.6bp (-13.6bp), May'25 -20.6bp (-19.5bp), Jun'25 -29.8bp (-28.8bp).

- No substantive reaction to this morning's housing and regional Dallas Fed services activity data. Looking ahead to Thursday data (prior, est): Initial Jobless (219k, 221k) and Continuing Claims (1.910M, 1.890M) at 0830ET; S&P Global US Manufacturing PMI (48.3, 48.3) at 0945ET; Construction Spending MoM (0.4%, 0.3%) at 1000ET.

- Treasury supply: $85B 4- & $80B 8W bill auctions at 1130ET, $64B 17W bill auction at 1300ET.

COMMODITIES: WTI Futures, Gold Holding Higher

WTI futures are trading higher today as the contract extends recent gains. A stronger reversal to the upside would refocus attention on key short-term resistance at $76.41, the Oct 8 high. Initial firm resistance is unchanged at $71.97. A bear threat in Gold remains present. The yellow metal traded sharply lower on Dec 18 and the move undermines a recent bull theme. A resumption of weakness would open key support at $2536.9, the Nov 14 low.

- WTI Crude up $0.9 or +1.27% at $71.88

- Natural Gas down $0.32 or -8.13% at $3.618

- Gold spot up $19.24 or +0.74% at $2625.86

- Copper down $6.95 or -1.7% at $402.3

- Silver down $0.1 or -0.34% at $28.8383

- Platinum up $3.96 or +0.44% at $908.02

US STOCKS: Late Equity Roundup: Tech & Interactive Media Sectors Underperforming

- Stocks are trading near session lows after reversing early session gains. Though off this year's record highs (SPX Eminis 6178.75, DJIA 45,073.63, Nasdaq 20,204.58) major averages will finish the year with double digit gains: SPX Eminis +19.5%, DJIA +13.1%, while the Nasdaq gained 29.9%!

- Currently, the DJIA trades down 92.19 points (-0.22%) at 42474.46, S&P E-Minis down 28 points (-0.47%) at 5929.75, Nasdaq down 147 points (-0.8%) at 19337.13.

- Information Technology and Communication Services shares underperformed continued to underperform late Tuesday, shares of software and semiconductor makers weighing on the tech sector: Nvidia -1.61%, Advanced Micro Devices -1.36%, Crowdstrike Holdings -1.28%.

- Interactive media and entertainment shares weighed on the Communication Services sector: Alphabet -0.9%, Live Nation -0.76%, Netflix -0.60%, Meta -0.41%.

- On the positive side, Energy and Materials sectors outperformed in the second half, oil & gas stocks buoyed the Energy sector as crude prices continued to rise (WTI +1.0 at 71.99): APA Corp +3.59%, Marathon Petroleum +2.46%, Occidental Petroleum +2.15%.

- Meanwhile, shares of chemical & fertilizer makers supported the Materials sector: Mosaic +2.44%, Celanese +1.42%, Dow +1.37%.

- Looking ahead, the next round of quarterly earnings kicks off mid-January with Blackrock, Bank of NY Melon, Wells Fargo, JP Morgan, Goldman Sachs, Citigroup, US Bancorp, M&T Bank and PNC all reporting between January 13-16.