PERU: Analyst Views Following Peru CPI

- *BBVA: Peru’s inflation continues to consolidate lower, strengthening confidence that headline and core CPI will settle at the 2.0% target. This has brought inflation expectations down, creating space for another cut by the BCRP as they fine-tune policy. Nevertheless, the central bank may still choose to be cautious in its approach for now, given the prevailing external uncertainties. BBVA’s USDPEN trade idea hit their trailing stop last month, triggering them to take profit. BBVA would still prefer to fade spikes in USDPEN and will likely re-engage closer to 3.68-3.70.

- *JP Morgan: Once controlled for food and energy, core CPI logged 0.64%m/m, with the annual rate converging to 1.86 %oya. in the same vein as for headline CPI, once adjusted for seasonality, the speed of travel runs below the 2%ar threshold, at 1.5%ar. In terms of CPI forecasts, the December 2025 projection is maintained at 2.3%oya, projection that assumes no relevant domestic supply shocks. JP Morgan’s forecast sits about 30bp above the point estimate presented by the central bank in the latest Inflation Report.

- *Goldman Sachs: The anticipated annual resetting of education tuition fees drove most of the variation in core prices, with higher-than-expected noncore pressures from the ongoing heatwave straining food supply. Firmly anchored within the target band, GS see Y/y headline CPI rising moderately in upcoming months on adverse base effects, ending 2025 at 2.4%. The benign inflation outlook does not constitute an impediment to the delivery of what GS view as the last 25bp rate cut during this cycle, which may be constrained instead by the volatile external backdrop.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

COMMODITIES: Recent Weakness Bolsters Bearish Outlook for WTI Futures

The current bearish trend condition WTI futures remains intact and last week’s sell-off reinforces a bear theme. The move lower has resulted in a clear breach of support at $70.20, the Feb 6 low. This confirms a resumption of the downtrend that started on Jan 15 and paves the way for an extension towards $67.75, the Dec 20 ‘24 low. Key short-term resistance has been defined at $73.33, the Feb 11 high. A corrective phase in Gold remains in play and the yellow metal traded lower last week. Price has breached the 20-day EMA, at $2879.8. This signals scope for a deeper short-term retracement, possibly towards the next important support around the 50-day EMA, at $2804.6. For bulls, a resumption of gains would refocus attention on the next objective at $2962.2, a Fibonacci projection. This would also open the $3000.0 handle.

- WTI Crude down $0.31 or -0.44% at $69.42

- Natural Gas down $0.02 or -0.63% at $3.811

- Gold spot up $11.21 or +0.39% at $2869.33

- Copper up $0.75 or +0.16% at $455.3

- Silver up $0.26 or +0.84% at $31.4227

- Platinum up $5.15 or +0.54% at $954.31

EQUITIES: Trend Condition in Eurostoxx 50 Futures Remains Bullish, For Now

The trend condition in the Eurostoxx 50 futures contract remains bullish and - for now - the latest shallow retracement appears corrective. The contract has pierced support at the 20-day EMA, at 5417.56. A clear break of this average would signal scope for a deeper retracement - note that the 50-day EMA lies at 5266.18. The EMA represents a key area of support. For bulls, a resumption of gains would open 5574.57 next, a Fibonacci projection. Recent weakness in the S&P E-Minis contract has resulted in a breach of a number of important supports; 6014.00, the Feb 10 low, and 5935.50, the Feb 3 low. The sharp move down signals scope for a deeper retracement and has exposed the next key support at 5809.00, the Jan 13 low. Clearance of this level would highlight a stronger reversal. On the upside, initial firm resistance to watch is 6038.96, the 50-day EMA.

- Japan's NIKKEI closed higher by 629.97 pts or +1.7% at 37785.47 and the TOPIX ended 47.47 pts higher or +1.77% at 2729.56.

- Elsewhere, in China the SHANGHAI closed lower by 3.972 pts or -0.12% at 3316.925 and the HANG SENG ended 64.95 pts higher or +0.28% at 23006.27.

- Across Europe, Germany's DAX trades higher by 187.69 pts or +0.83% at 22736.32, FTSE 100 higher by 25.03 pts or +0.28% at 8834.53, CAC 40 up 28.59 pts or +0.35% at 8138.46 and Euro Stoxx 50 up 16.61 pts or +0.3% at 5479.27.

- Dow Jones mini up 43 pts or +0.1% at 43929, S&P 500 mini up 12.75 pts or +0.21% at 5975.75, NASDAQ mini up 69.5 pts or +0.33% at 20987.

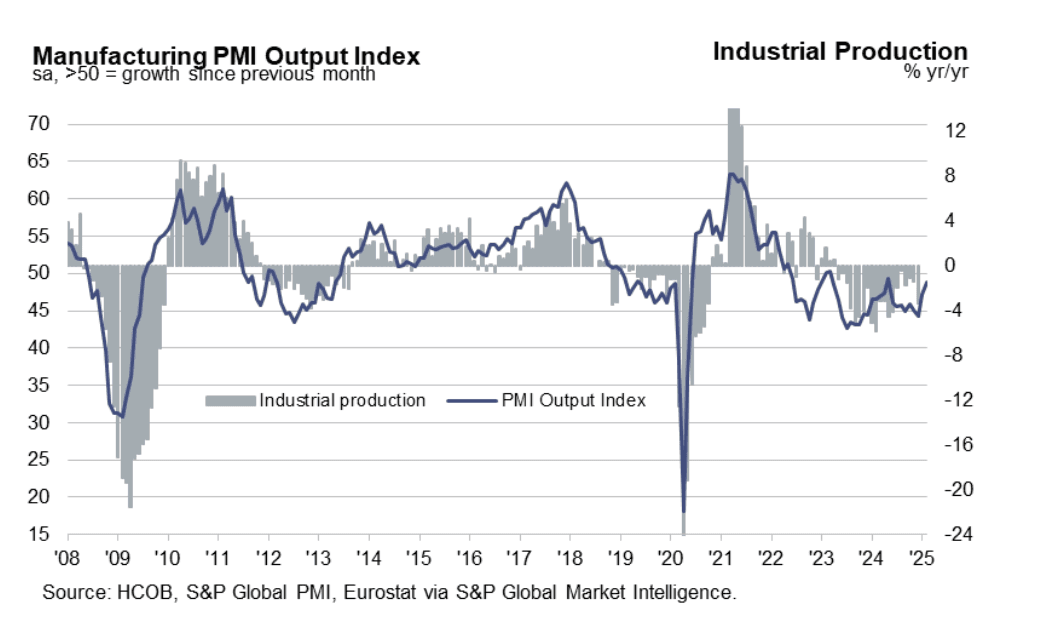

EUROZONE DATA: Weaker Employment A Theme In Feb Manufacturing PMIs

The Eurozone February manufacturing PMI saw a small upward revision to 47.6 (vs 47.3 flash, 46.6 prior), following upward revisions to the French and German prints and a stronger-than-expected Italian reading. From the report “Factory production came close to stabilising, with reductions in new orders – both total and from abroad – at their softest in nearly three years”.

- However, a theme across the four major Eurozone economies was weaker employment: “Eurozone factories continued to cut their workforces, however. The rate of job shedding even accelerated, reaching its most substantial in four-and-a-half years”.

- On prices, Germany was an outlier in reporting falling input cost pressures. For the Eurozone overall: “Cost pressures facing eurozone factories intensified midway through the first quarter as the rate of input price inflation quickened to a six-month high. The latest data implied that these greater expenses were absorbed by companies as output charges were discounted marginally since January”.

- Confidence in the year-ago outlook nonetheless improved (albeit from a very low base): “The outlook for factory production over the next 12 months remained positive, with eurozone manufacturers predicting growth. Furthermore, the level of optimism was among the highest seen since Russia’s full-scale invasion of Ukraine three years ago”.